Best Business Credit Cards for Startups (2025): Top 5

If you are launching a startup or new business in 2025, one of the smartest moves you can make is getting the best credit card for your setup. This guide helps you pick the two best business cards for your startup by matching rewards and protections to your actual spend and cash-flow—not nine cards you’ll never use. You’ll get simple math, clean comparisons, and a step-by-step path. Moreover, no debt and no bloat—just the facts so you can make the best decision for you.

But before we dive in, I want to paint a picture for you. You just landed your first $4k client. The ad buy is due Friday, your phone bill hits Tuesday, and that laptop you’ve been limping along with—well, let’s just say that it’s not making it until next month. This is the moment where two right business cards take chaos off your plate—and pay you back for the spend you already have.

Disclosure & Glossary

Disclosure: Some links (Amex only) may earn MMF a commission if you’re approved—at no extra cost to you. This post is for education only, not financial advice. Terms apply. Rates, fees, benefits, and welcome offers change frequently. Always verify details on the issuer page before applying.

Glossary: UR = Ultimate Rewards, MR = Membership Rewards, AF = Annual Fee, NPSL = No Preset Spending Limit.

Jump to

- Why Get a Business Credit Card for Your Startup

- The Best Card for You

- Comparison Table

- Protections and Purchase Insurance at a Glance

- Tips to get approved for Business Credit Cards

- Top 5 Best Business Credit Cards

- Best Business Credit Card Duos for Startups

- Takeaways/ FAQ

TL;DR (6 picks + when to choose it)

Quick heads-up: the Amex links below are referral links. If you’re approved, I may earn points or a statement credit—no extra cost to you. Applying through my link helps support this blog, so thanks in advance. Offers change; please check the issuer page.

Best overall

Chase Ink Business Preferred® — 3× on shipping, select online advertising, travel, and internet/cable/phone (up to $150k per account year, then 1×); 1:1 UR transfers; cell-phone protection; primary rental CDW for business rentals. When to choose it: You buy ads and want optional point transfers. (Welcome offer/details: see issuer page.)

Best cash-flow/float:

The Plum Card® from American Express — choose up to 60 days to pay on eligible charges or take a 1.5% Early Pay Discount; NPSL; Pay Over Time if enrolled. (Details and eligibility vary—see issuer page.)

Best premium travel:

The Business Platinum Card® from American Express — 5× on flights and prepaid hotels booked at AmexTravel.com; Global Lounge Collection access; 1.5× on select categories or on purchases ≥$5k; NPSL; Pay Over Time if enrolled. (Benefits/credits subject to terms.)

Best simple earn (no AF):

Chase Ink Business Cash® or Amex Blue Business Plus — Chase Ink Business Cash® or Amex Blue Business Plus — Ink Cash: 5% at office supply stores and on internet/cable/phone (combined $25k per account year, then 1%); 2% at gas and restaurants ($25k cap); BBP: 2× MR on first $50k per calendar year, then 1×.

Best ads & SaaS flexibility:

American Express® Business Gold — 4× on your top 2 eligible categories each billing cycle (up to $150k per calendar year, then 1×)

BONUS!: Best Credit-building (unsecured):

Capital One Spark Classic — $0 AF; 1% back everywhere; 5% on hotels/cars via Capital One Travel. When to choose it: You’re sub-700 and need an unsecured on-ramp; note business activity is commonly reported to consumer bureaus—confirm with issuer for your specific card.

Rule of thumb: Points = flexibility (if you travel). Cash back = simplicity (if you don’t). And always autopay in full.

Why should you get a business credit card for your startup or small business?

Cash-flow Advantages

Business credit cards offer immense flexibility and benefits when it comes to getting your new business up and running. For example, using credit cycle timing smartly, you can smooth cash flow and make necessary purchases—always with autopay in full to avoid interest.

With this strategy, it’s extremely important that you have a good handle on your cash flow, risk, and how your business operates. The goal here is not to take on as much debt as possible; instead, it’s to use that debt smartly to maximize your revenue.

Cash back and travel benefits

Beyond cash flow, rewards are the other big reason startups turn to business cards. By using business credit cards instead of debit cards, new entrepreneurs can receive various benefits from credit cards, including cashback, travel points, which can be redeemed for flights or hotels, and other benefits and credits.

Strong Welcome Offers

Additionally, business credit cards typically have higher spend requirements and welcome offers versus personal cards, so high-spending startups can extract even more value. When I first began my ATM business, I used my Amex Blue Business Cash to purchase my ATM. Although I had the money in my bank account, this allowed me to get 2% back on a $3,000 purchase.

Credit impact & Chase 5/24 basics

When you apply for a business card, it’s worth knowing how issuers treat personal credit reports and the Chase 5/24 rule—two factors that can shape your approval odds.

Minimal effect on your Personal Credit Report

Understanding how business credit cards affect your personal credit score is very important. Generally, business credit cards, like American Express and Chase, have little to no effect on your personal credit report so long as your account stays in good standing. Because of this, your utilization and number of credit accounts are rarely reported. This is extremely beneficial when pairing business credit cards with personal ones to avoid going over certain issuers’ application guidelines, like Chase’s “5/24.” (Guidelines vary by issuer and can change.)

Chase 5/24 – What is it?

The Chase “5/24” rule is an unpublished guideline widely reported by applicants: having 5 or more new personal accounts in the past 24 months often leads to automatic denials for new Chase personal cards. As of August 26, 2025, there’s no official change published; recent datapoints suggest most business cards do not add to your 5/24 count, but policies and reporting can vary. Therefore, always check recent datapoints before applying. Most business credit cards require a hard inquiry pull, so that is something to be mindful of, as too many hard pulls in a short period of time will hurt your credit score.

Separating business and personal expenses

In addition, business cards keep your books cleaner by splitting personal from business purchases. Come tax season, your accountant will thank you for this.

Building Business Credit

Business credit cards for your startup or small business will help you build up your business credit. This will come in handy in the future applying for new business credit cards or loans

Who Qualifies for Business Credit Cards?

Whether you have an LLC or are a sole proprietorship, you’d be surprised to know that many people actually qualify for business credit cards. Even if you do not have an LLC set up or an EIN, you can still qualify for a business credit card if your side hustle is considered a business. Some good examples of this would be content creation like YouTube, eBay reselling, ATM and Vending machine businesses, Etsy selling, and more. Likely, if you make any side income or project to make any side income, you have a good chance of qualifying.

Choosing the Best Business Credit Card for You

How to choose (quick checklist)

- Do you want cash back (simple) or points (flexibility for travel)?

- Will you use premium perks (lounges/credits), or keep it simple?

- Do your top categories stay the same (Ink Preferred) or rotate (Amex Business Gold)?

- Do you need float (Plum) or a 0% intro window for a specific purchase?

- Are you okay with an annual fee, or do you want $0 AF?

For this list, assume a 700+ credit score. If you’re below that, see the bonus “builder” option and the quick score-lift tips below. Don’t worry if you are under 700, I’ve added a bonus card that would be perfect for you. There are also a few tips you can take to raise your credit score, so you’ll be in the perfect position to apply for one of the other 5 cards.

The Road Map For the Best Business Credit Cards for Startups

Need float?

If receivables land 30–60 days after kickoff, consider Plum: either use the Extra Days to Pay (on eligible charges) or take the 1.5% Early Pay Discount when cash arrives early. Prefer a defined runway for a specific buy? If shown on the issuer page, a 0% intro APR purchase window (e.g., Ink Cash/Ink Unlimited) lets you amortize—only if you’ll clear it before promo end.

Buy ads/SaaS/ship/telecom?

That’s Ink Business Preferred (3×) vs Amex Business Gold (4× top-2 to $150k/yr). If your spend stays in those 3× lanes and you want UR transfers, go Ink Preferred. If your top two categories change month-to-month, Business Gold auto-adapts.

Airport life?

Amex Business Platinum makes airports civilized: lounges, 5× flights & prepaid hotels via AmexTravel, plus 1.5× on eligible large/select purchases. If you don’t travel or won’t use credits, skip it.

Keep it simple?

You won’t miss with Ink Cash (5% at office supply + internet/cable/phone, caps apply; $0 AF) or Blue Business Plus (flat 2× MR to $50k/yr, then 1×). Prefer flat cash back? Ink Unlimited (1.5% everywhere) is the “no spreadsheet” option.

Before you apply: Run our Free Credit Card Approval Checker. Education only. Terms apply.

Want a broader plan? Skim How to Build Wealth (Beginner’s Guide)

Appendix: the original decision tree (tap to open)

Need breathing room on cash? → Plum or a 0% intro purchase window (if shown).

Heavy ads/SaaS/ship/telecom? → Ink Preferred (3×) or Biz Gold (4× top 2).

Airport life? → Biz Platinum (lounges, 5× AmexTravel); otherwise skip.

Simple baseline? → Ink Cash, BBP 2×, or Ink Unlimited 1.5%.

The Best Business Credit Cards for Startups: Key Factors at a Glance

| Card | Annual fee (as of date) | Top earn & caps | Key benefits | Who it’s for |

|---|---|---|---|---|

| Chase Ink Preferred | $95 | 3x ads, travel, shipping, internet/phone; cap. | Point transfers to airline/hotel partners. | Creators, agencies, e-commerce with ads. |

| AmEx Plum | $250 | Pay up to 60 days or 1.5% early. | Flexible payment terms; no preset limit. | Contractors, projects needing flexible float. |

| AmEx Business Platinum | $695 | 5x flights/prepaid hotels; 1.5x large purchases. | Global lounges; travel and purchase credits. | Frequent flyers; consultants using lounges. |

| Chase Ink Cash | $0 | 5% internet/phone, office; 2% gas/restaurants. | Pairs with Ink Preferred for transfers. | Local services; lean teams paying bills. |

| AmEx Business Gold | $375 | 4x top two categories; yearly cap. | Monthly credits; Pay Over Time optional. | Ads, software, shipping, wireless spenders. |

| AmEx Blue Business Plus | $0 | 2x points on first $50k yearly. | Simple earning; easy points pooling. | Minimalists wanting simple two-times earn. |

| Chase Ink Unlimited | $0 | 1.5% back on all purchases. | Flat rate; pairs with Ink Preferred. | Flat-rate simplicity for everyday spend. |

| Capital One Spark Classic | $0 | 1% back; 5% hotels and cars. | Unsecured starter for fair credit. | Sub-700 builders; thin files. |

Education only. Terms apply. Never carry a balance—set autopay in full.

The Best Business Credit Cards for Startups: Protections at a glance

Note: Coverage varies by card. Always read the Guide to Benefits for specifics.

- Ink Business Preferred: Cell-phone protection (up to $600 per claim, 3 claims/yr), purchase protection (120 days, up to $1,000/claim), extended warranty (adds 1 year), and primary rental car CDW for business use.

- Plum (Amex): Limited coverage: AmEx purchase protection (90 days, up to $1,000/item) and secondary rental coverage. No cell-phone protection.

- Amex Business Platinum: Premium protections: trip delay/cancellation, baggage insurance, purchase protection (90 days, $10k/item up to $50k/yr), extended warranty (adds 1 year), and premium rental car coverage.

- Ink Business Cash: Purchase protection (120 days, up to $500/claim), extended warranty (adds 1 year), and secondary rental CDW for business use.

- Amex Business Gold: Purchase protection (90 days, up to $1,000/item), extended warranty (adds 1 year), and standard rental coverage.

- Blue Business Plus: Purchase protection (90 days, up to $1,000/item) and extended warranty (adds 1 year).

- Ink Business Unlimited: Purchase protection (120 days, up to $500/claim), extended warranty (adds 1 year), and secondary rental CDW.

- Spark Classic: Basic purchase protection (90 days, up to $500/item) and secondary rental CDW. No extended warranty or cell-phone coverage.

Tips for Applying for Business Credit Cards

- New LLC? (<12 months): Lay out your cash on hand, clear use case notes, and projected revenue.

- Sole Proprietorship without an EIN? Apply under your legal name with your SSN (be accurate and consistent)

- High Utilization This Month? Pay balances down before you apply; aim for less than 30% minimum (ideally less than 10%)

Use my Free Approval Checklist for the key items to review before applying.

The Best Business Credit Cards for Startups (Top 5 + a Bonus)

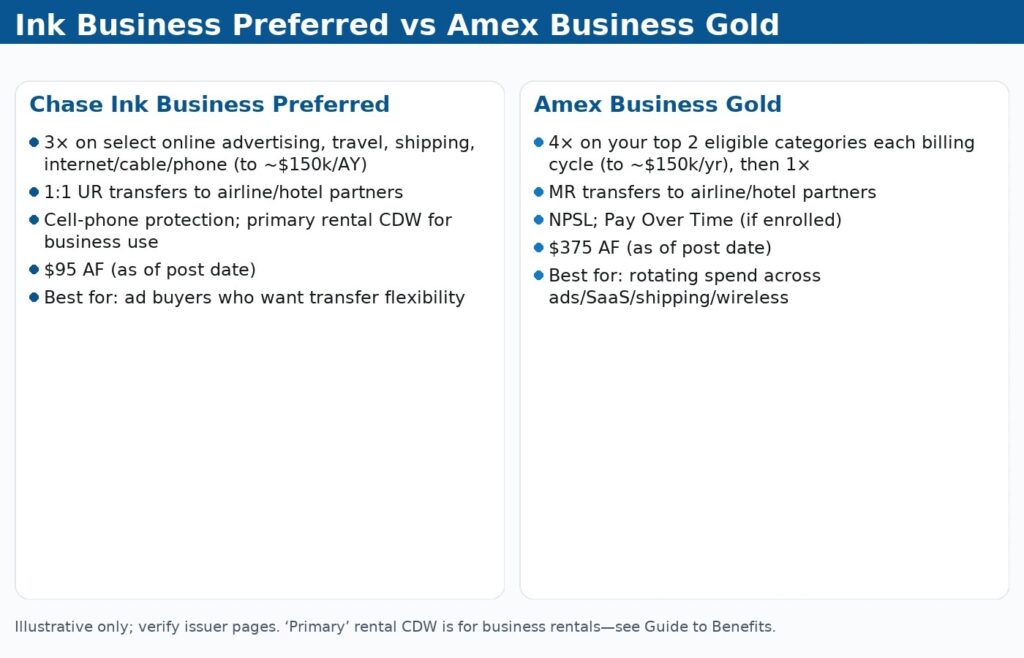

Chase Ink Business Preferred® – The Best All-Arounder

The Chase Ink Business Preferred is comfortably one of the best business credit cards for startups. Its main multipliers are 3× on ads, telecom, shipping, and travel, plus 1:1 UR transfers when you want more value. This makes it a great fit for creators, agencies, and e-commerce businesses running ads or for teams who travel often and benefit from airline and hotel partners. On the other hand, it’s not recommended for startups that won’t use transfer partners or maximize the 3× categories. A smart pairing is to add Ink Cash for 5% on bills, pooling UR into Preferred before transferring. For example, $5,000 per month on eligible ads × 12 months at 3× = 180,000 UR per year (~$1,800 at 1.0¢ value, potentially higher with transfers).

American Express® Business Gold – The Two Category Spender

The AmEx Business Gold adapts as your spending shifts, awarding 4× on your top two eligible categories (up to $150k per year). It is especially useful for paid-media buyers and software-heavy teams with rotating top expenses. By contrast, it is less useful for businesses with flat or low spend, who may prefer the Blue Business Plus at 2×. A solid strategy is to pair it with Business Platinum for travel perks while keeping BBP for everyday “everything else” spend. As an illustration, $3,000 per month split between ads and SaaS at 4× = 144,000 MR per year.

The Plum Card® from American Express – Best for Cash Flow Flexibility

The Plum is the most black and white out of all of them, but it needed to be on this list. It’s not for everyone, but for businesses with seasonal or invoice-based cash cycles, it can be a standout. If you are a seasonal, retail, or construction, this card is the perfect card. Delaying and setting your own payment terms out to 60 days can allow you to scale and operate at so much more of an efficient level. For everyone else, though, this card is a hard pass.

Why it’s great: Choose up to 60 days to pay on eligible charges or a 1.5% early-pay discount—whichever fits the project. That said, avoid stretching past the extra-day window; set autopay & calendar reminders

Who it’s for: Contractors, event producers, and inventory-heavy teams with predictable receivables.

Don’t get if: Anyone tempted to stretch past 60 days.

Top pairings: Use Plum for vendor float; route daily spend to Blue Business Plus (2× up to $50k/yr).

Basic Example: Pay $10,000 within 10 days of statement close → $150 discount.

Note: Float is a tool—add autopay and calendar reminders.

The Business Platinum Card® from American Express – Best Premium Travel Card for Startups

The minimum spend on this thing to hit the welcome offer is insane, but if you have a business pushing out that much spend, this card is for you. Amex has been getting a lot of hate as of late as a glorified coupon book, but they still do premium business cards the best out of any other issuer. If you travel often for your startup, then this is a card worth looking into.

It’s important to note that while the annual fee on this card is high, you should be looking at your effective annual fee when judging a card. Effective annual fees are the total annual fee, the value you assign to the use of credits and perks naturally. Key there is naturally. If you have to go out of your way to use a credit card somewhere, that is not worth it.

Key multipliers: 5× on flights & prepaid hotels via AmexTravel; 1.5× on eligible categories or ≥$5k purchases; lounges smooth travel days.

Perfect choice if: Road-warrior founders and startup entrepreneurs who’ll actually use lounge access and credits.

Who it’s NOT for: Rare travelers; AF-sensitive businesses.

Best uses & pairings: Pair with Business Gold (4× top-2) for earn; redeem MR for flights/hotels as needed.

Simple Real World Example: $12k equipment in a 1.5× bucket → 18k MR; add 5× on flight/hotel bookings.

Chase Ink Business Cash® – Best 5% Specialist Card

Anyone who loves the points and miles game knows how coveted a 5% category specialist is. Ink Business Cash gives you that on two categories (office supply; internet/cable/phone) plus two 2% on gas and restaurants, each with annual caps. As a standalone, I think there are better cards out there than this one, but combined with the Ink Preferred or even some Chase personal credit cards and you’ve got a spicy trifecta/duo that will be able to stand up to any credit card set-ups.

Best features: 5% on internet/cable/phone + office (first $25k/AY), 2% gas/restaurants (first $25k/AY), $0 AF; often 0% intro APR 12 mo purchases if shown.

Who it’s for: Local services and lean shops that pay real-world bills.

Who it’s NOT for: Teams chasing lounges/elite travel.

Best uses & pairings: Pair with Ink Preferred to unlock UR transfers; or add Ink Unlimited for baseline 1.5%.

Simple Real World Example: $800/mo telecom + $600/mo office = $1,400 at 5% → $840/yr.

Amex Blue Business Plus – The Simple Catch-all

For smaller businesses looking for a simple 1-card setup, the BBP offers a simple and clear rewards structure with no annual fee. This reward structure is perfect for anyone looking to dip their toes into the points and miles game without diving headfirst. Where I would use this card, however, is as a catch-all to pair with another card, ideally staying in the Amex ecosystem. This will give you a specialist and catch-all in the same ecosystem to stack rewards over time.

Why it’s great: 2× MR on the first $50k/yr (then 1×), $0 AF; often 0% intro purchases 12 mo if shown.

Who it’s for: minimalists who want steady value without categories.

Who it’s NOT for: founders chasing high multipliers in specific lanes.

Best uses & pairings: anchor with BBP, then add Ink Cash for 5% bills or Ink Unlimited for 1.5% everywhere.

Math you can copy: $2k/mo at 2× = 48k MR/yr (~$480 @1.0¢).

Capital One Spark Classic – For the Credit Builder

If your credit score is lower than 700, you might find it difficult to get approved for some of the cards on this list, but that’s where the Spark comes in. Sure, this isn’t the best card from a rewards perspective, but it gets you moving in the right direction. Take the 1x back everywhere, plus the 5x back using the travel portal, and work on building your credit. Make sure you are paying off your balance in full monthly and keeping your utilization low, and your score should start rising over the coming months.

Why it’s great: $0 AF, 1% back everywhere; 5% on hotels/cars via Capital One Travel; unsecured option for sub-700 profiles.

Who it’s for: builders who need a starter line without a deposit.

Who it’s NOT for: anyone who must avoid personal reporting (Capital One business activity is typically reported to consumer bureaus; confirm for your specific card).

Best uses & pairings: keep utilization low, autopay in full; later upgrade to Ink/Amex multipliers.

Math you can copy: $2k/mo at 1% = $240/yr (+ $100 if $2k via C1 Travel at 5%).

The Best Business Credit Card Duos for Startups

Ads + sometimes travel? — Ink Preferred + Ink Cash

- 180,000 UR from ads (3×) ≈ $1,800 @1.0¢ (to $2,700 @1.5¢; value varies)

- $840 from telecom/office (5%)

- AFs: Preferred ($95/yr), Cash ($0) → Net Yr-1: $2,545–$3,445 (approx., assuming typical AFs)

Takeaway: If you buy ads and pay for phone/office, this duo usually pays for itself—fast

Cash-flow breathing room? — Amex Plum + Blue Business Plus

- Early-pay savings: $900 (six $10k early payments @1.5%)

- 48,000 MR from BBP 2× ≈ $480 @1.0¢ (to $720 @1.5¢; value varies)

- AFs: Plum ($250/yr), BBP ($0) → Net Yr-1: $1,130–$1,370 (approx.)

Takeaway: Float + 2× keeps projects moving while you wait for invoices.

Minimalist? — BBP + Ink Cash or Ink Unlimited

- BBP: 48,000 MR ≈ $480 @1.0¢ (treat MR as 1.0¢ for simplicity)

- Ink Cash: $840 from 5% bills or Ink Unlimited: ~$360 from 1.5% on $24k

- AFs: $0 for both → Net Yr-1: $1,320 (BBP+Cash) or ~$840 (BBP+Unlimited)

Takeaway: Easiest path if you don’t plan to transfer points.

Takeaways

In short, you only need one to two solid cards that match your spending and cash flow. After you build your core setup, consider niche hotel/airline cards for welcome offers. For your core setup, if ads are your engine, go Ink Preferred or Amex Business Gold; if you live in airports, Business Platinum; if you need breathing room, Plum; if you want simple, Ink Cash or Blue Business Plus. These are proven ways to get value every day. Now, go run over and grab your free credit card checker; it will help you with your approval odds to make sure you lock in the perfect stack for you. Get the Free Approval Checklist →.

Ready to apply? Pick the Amex that fits your spend.

From our TL;DR picks, here are three strong Amex options founders often choose:

These are Amex referral links—if you’re approved, I may earn points or a statement credit at no extra cost to you. Offers change; always verify on the issuer page.

Chase Ink Business Preferred (3× on select ads/telecom/shipping/travel) is a top pick if you want partner transfers. If your top categories change monthly, Amex Business Gold (4× on your top two categories up to a yearly cap) fits better.

Amex Blue Business Plus earns 2× on everyday purchases up to the first $50k per calendar year, then 1×. It’s the easiest no-category setup.

It depends on the issuer. Most report only serious delinquencies, while Capital One typically reports all business activity to consumer bureaus—confirm with the issuer before applying.

Many sole proprietors are approved with modest or projected income. Be honest about current and expected revenue, explain your plan, keep utilization low, and always pay in full.

Make Sure You’re Ready to Apply

Use my free Approval Confidence Checklist to confirm you’re set up for the best chance of approval before applying for your next credit card.

Check your approval readiness here →