How to Pay Off Debt with Little Income: 9 Proven Strategies

If you’re grinding through life, living paycheck-to-paycheck, and wondering how you’ll ever pay off debt on a small income, you’re not alone, and you’re absolutely in the right place.

Here’s the reality: as of mid‑2025, the average person is carrying about $39,075 in student loan debt , according to Bestcolleges.com —that could cover groceries for a year if you’re short on income. Meanwhile, the average credit card debt? Hanging around $7,321 per person and climbing fast . That’s enough to make anyone’s heart race, and if every dollar counts in your world, the weight of it can feel crushing.

But here’s why you’re in the right place: I’ve built this guide specifically for folks earning less but determined to break free. I’m talking 11 realistic strategies that actually move the needle when it comes to understanding how to pay off debt with little income. We’ll walk through easy-to-understand tools like snowball vs avalanche debt strategies, automating payments, creating your own debt-freedom fund, and even how to squeeze extra income from the weirdest places.

By the end, you’ll have a simple, actionable plan that fits your budget and your life. Because paying off debt isn’t about magic or luck, it’s about having a smart system and celebrating each small win along the way.

TL;DR

- Build a one-page Debt Snapshot (balances, APRs, minimums, due dates).

- Pick Snowball (fast wins) or Avalanche (lowest interest cost).

- Autopay minimums + add $5–$25 extra to your priority debt each payday.

- Use a Hardship & Relief Toolkit (payment plans, negotiation, nonprofit counseling) to free cash flow.

- Track one micro-win per week to stay motivated.

1. Start With Complete Debt Clarity

Track Every Dollar (Even the Small Ones)

Being strapped for cash means losing sight of where your money goes; even $5 here or there adds up fast. That’s why starting with debt clarity isn’t optional—it’s essential. Take one night and write down all the debt you owe: student loans, credit cards, personal loans, and even that irritating overdraft. This can feel overwhelming, but it gives you the most important thing you need: a starting point.

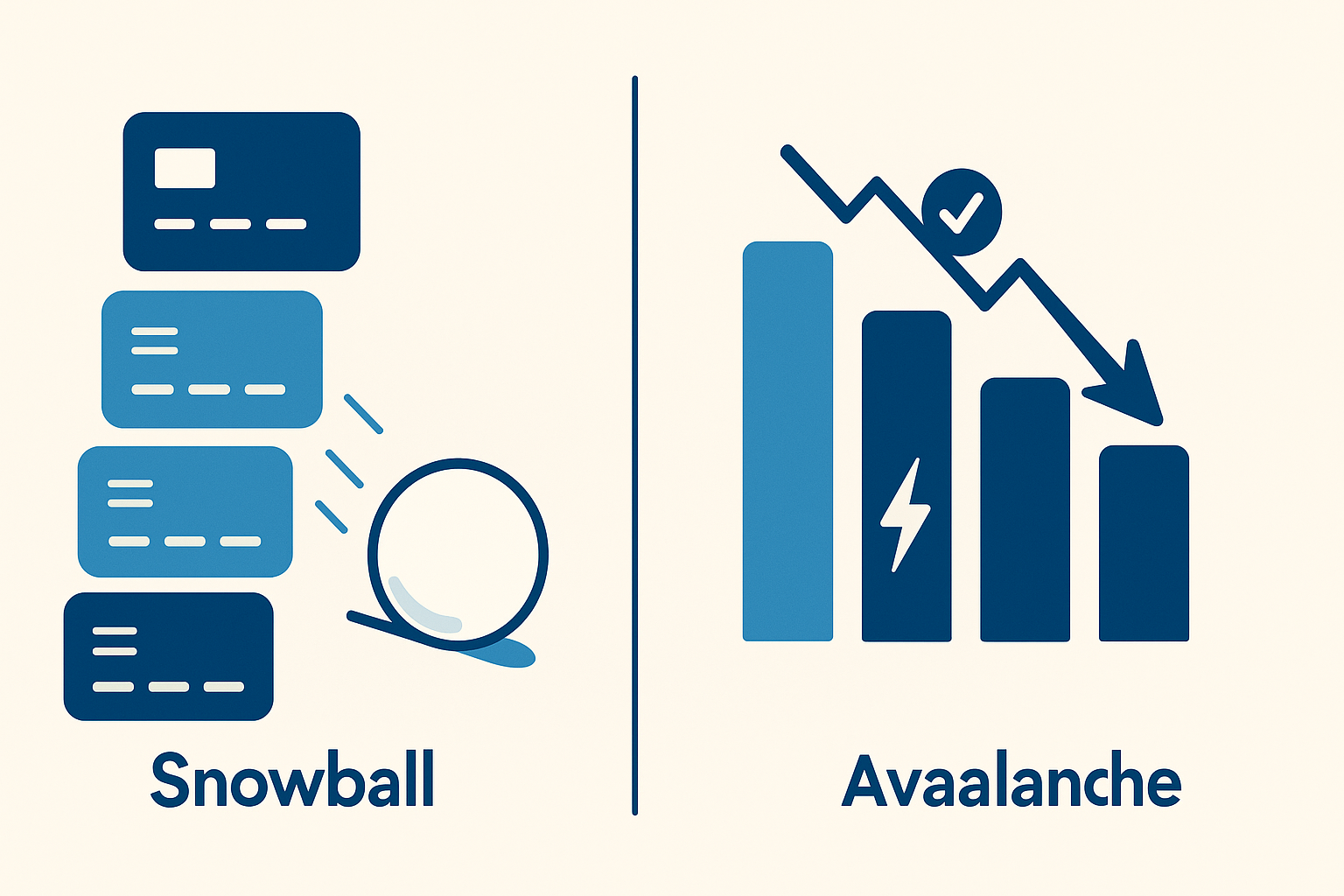

2. Pick Your Payoff Strategy: Snowball vs. Avalanche

Understanding your debts isn’t enough; you need an actionable game plan. That’s where snowball versus avalanche comes in. The snowball and avalanche strategies are two debt repayment strategies, but they emphasize repayment in different ways.

Snowball vs Avalanche Table (Pros, Cons, When to Use)

| Strategy | Best For… | Pro | Con |

|---|---|---|---|

| Snowball | People who need quick wins to stay motivated | Quick wins build momentum and confidence | May pay more total interest vs. Avalanche |

| Avalanche | Math-first folks focused on minimizing interest | Saves the most money on interest long-term | First “win” takes longer, which can hurt motivation |

Choosing your method is less about “the right one” and more about what keeps you going on the right track. If seeing that first balance drop gives you fire, snowball’s your friend. If math is your comfort zone and you don’t mind slower progress, Avalanche is where money gets saved fast.

3. Automate Minimums—and Sneak in Extra Payments

Once you have clarity and a strategy, automation is your secret weapon—especially when money’s tight. Having an understanding of your spend is key, but once that’s established, automation takes the guesswork and effort out of paying off debt.

Why Even $5 Extra Matters

Set up autopay for every minimum payment so you never miss one. Then, when you can spare a little extra—$5, $10, whatever—send it to your highest-priority debt today.

Those small extras don’t seem like much, but they shrink your balance faster and lower your interest charges. That compounding is what’s going to help you pay off debt faster with little income. Over time, those tiny wins add up, and keeping it automated means you’re making progress even when you’re too tired to think.

4. Cut Costs That Actually Add Up—No Guilt Required

Trim Smart, Not Scarcity-Style

Living on a tight budget means you can’t afford luxury hacks, but you can still trim expenses strategically. I’m talking subscriptions you never use, cable packages you don’t watch, and even planning grocery swaps. According to Credit Canada, low-income strategies often start with these simple cuts: “Cut unnecessary expenses,” “Avoid taking on new debt,” and “Create a detailed budget.”

Don’t think of this as “giving up something”. Instead, you’re trading small, poorly used costs for big, long-term wins. Every dollar saved funnels straight into debt freedom.

5. Refinance, Consolidate, or Transfer—But Only If It Fits Your Situation

When Refinancing or Transfers Help (And When They Don’t)

Sometimes, smarter structuring beats brute savings. Refinancing, consolidation, or balance transfers can lower your interest rate—if done correctly.

- Refinancing gives you the ability to get a more favorable rate or term that better fits your income .

- Debt consolidation or transfer can simplify your life by going from 10 payments per month to one—but watch out for fees and qualification requirements.

In essence: structure smarter, but don’t let the simplicity justify sinking fees or worse terms.

6. Use Unexpected Gains (& Tiny Wins) to Make a Big Dent

Surprise Your Debt Reckoning

Ever had a random $20 from a refund, birthday card, or side gig? Before you spend it, take a breather. Figure out what’s the best use of that money— that answer may be surprising, your debt with it. I remember one month, I got a $50 rebate for contacts that felt insignificant. I took weeks to submit it, and I wasn’t even sure I was going to get it.

Then I turned that money around to pay off a part of a trip I used on my travel credit card. Suddenly, my motivation flipped. It’s not about having a windfall—it’s what you do with every small win that matters. That’s one of the core strategies to pay off debt faster with little income.

Those surprise “free” bucks add up, especially when they’re forced into automation. Make it a mini win with no thought required.

7. Lean Into the Power of Small Hustles—I’m Talking Dollar-a-Day stuff

$1 a Day Turns Into $365 a Year

Is $365 a life-changing amount of money? Maybe for some more than others. But can you make 7$-20$ per week with side hustles? Easily, with the right approach. A side hustle doesn’t have to be full-time. I normally spend a few hours on a Saturday or Sunday morning thrifting and listing stuff on eBay. This nets me between $25-$100/week and helps cover most of my credit card charges. Whether it’s flipping furniture on Facebook Marketplace, selling notes, or micro-jobs, one small task a day builds momentum.

Once your side hustle is established, you can add value even further by leveraging a business credit card to maximize cash back and rewards from business purchases, even if the side hustle is not an official LLC. It’s important to remember that this is not a technique to increase your debt; the goal here should be maximizing the spending you are already making. Always pay your credit card off in full and set auto pay.

8. Celebrate Every Win—Big or Small

Success Doesn’t Have to Be Epic – Small Wins Compound Over Time

Debt freedom isn’t built on giant leaps—it’s built on small steps. Did you get a $20 refund and use it to chip away at your balance? That’s progress. Paid off a $50 bill? That’s a solid win. Keep that mentality, and you will be successful in the long term.

Creating space to recognize these micro-victories makes this journey sustainable. Think about DIY visuals like a sticky note chart, a Pinterest board overlay, or a “Debt Meter” in your phone background.

9. Fix Habits to Avoid Getting Back in the Hole

Build Your “Debt-Free Life” Blueprint

You’ve hustled, you’ve moved, you’ve eliminated some balance—and now it’s time to create a life that keeps you debt-free.

- Step 1 – Plug the hole: Stop impulse buys by unsubscribing from sale emails, deleting saved card details, or unsubscribing from ads on Amazon.

- Step 2 – Set guardrails: Map out your monthly spend and debt repayment schedule while also taking into account personal spending, so that you work towards your financial goals without sacrificing your life today

- Step 3 – Stay Disciplined: Envision how debt freedom feels. A small vision board or daily affirmation can be surprisingly powerful.

It’s not about shame—it’s about designing your environment so that the “pull” of debt stays weak, and the “pull” of freedom stays strong.

Shout out to you—reading this far with intention and grit. That means you’re not just wishing debt away—you’re making a real plan and moving forward. That matters.

Here’s what to do next:

- Pick one strategy from above—snowball, automation, mini hustle—and test it this week.

- Use your “secret found money” wisely—refunds, bonuses, side gig cash—drop it right into your highest-priority debt.

Once your debt starts shrinking, it’s powerful to pivot toward building wealth—check out the beginner’s guide on how to build wealth with assets to lock in momentum and grow your long-term financial foundation.

Working to pay down debt with little income isn’t a sprint—it’s a marathon of micro-wins, consistent action, and tough kindness toward yourself.

Let every small step forward remind you: you’re rewriting your money story—and that’s everything.

Absolutely. This is about strategy, not magic. Smart budgeting, consistent systems, and small hustles all add up over time. You’ve got the power in your hands—and your heart.

Use whichever one keeps you moving. Snowball gives you quick wins. The avalanche strategy saves more interest. Pick the one that helps you stick to the plan.

Yes—especially if you start with a mini emergency fund. Take it slow, prioritize paying down debt, but do both if you’re up for the challenge, you’ll be better off for it.

Break it into chunks. Set small goals like “Pay $250 by month-end.” Give yourself visual reminders and small rewards to keep motivation strong.