How to Build Wealth with Assets (A Beginner’s Guide 2025)

As a young person trying to find your footing financially, one of the best goals you can focus on is learning how to build wealth with assets. This approach is one of the strongest wealth-building strategies for beginners because assets are the key to growing your net worth. Many wealthy people understand this, which is why you’ll often see them buying inexpensive or fully paid‑off cars instead of extravagant leased cars. Why? First, it’s a smart financial decision that signals living below your means. Second, it reflects an understanding of the value of owning long‑term assets versus paying for depreciating ones.

In this post, I’ll break down what assets are, the different types you should know, why they matter, and practical ways young investors can start accumulating them early to build lasting wealth.

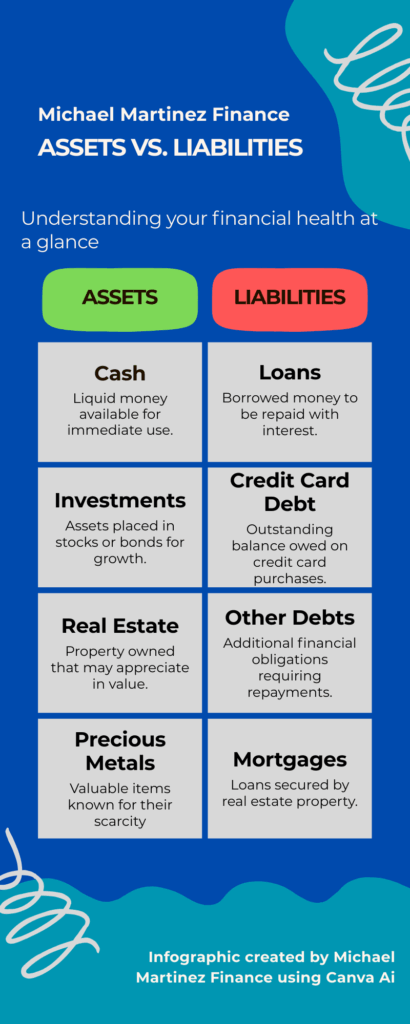

Assets vs. Liabilities (Fast Definition)

At its core, personal finance is a balancing of assets vs. liabilities to maximize what you own and minimize what you owe.

- Assets: Things you own that have value (cash, investments, property, equipment, skills, intellectual property).

- Liabilities: Obligations you owe (debt, loans, unpaid bills).

- Goal: Grow assets, manage liabilities, and widen the gap over time.

What Are Assets and Why Do They Matter for Young Investors?

Simply put, assets are the building blocks for growing wealth. They can be anything from money to your home to a business or skill you own. Generally, assets either appreciate (increase in value) or depreciate (decrease in value). Value can come from scarcity (e.g., precious metals), utility (e.g., income‑producing equipment), or the work invested to create them (e.g., intellectual property).

Types of Assets

Tangible Assets Every Young Investor Should Consider

Tangible assets are physical—things you can touch, see, or hold. Examples include:

- Real estate: Potential for appreciation and/or cash flow.

- Precious metals: Scarcity value; a store of value.

- Equipment/vehicles/tools: Utility that can produce income.

These are the most common starting points for young investors looking to build wealth with assets.

Intangible Assets and How They Can Boost Wealth

Intangible assets are non‑physical, like intellectual property (patents, content, code), brand value, and goodwill. They matter a lot when evaluating companies as an investment. For individuals, the skills you build along with certifications, portfolio projects, and content libraries are intangible assets. These are unique attributes that make you you and can help drive income.

Why Learning How to Build Wealth With Assets is so Influential

Understanding how to build wealth with assets is extremely important for anyone pursuing financial freedom. Assets give you stable, long-term growth potential and the ability to create income streams that work for you.

- Net Worth: Assets directly drive net worth. The more quality assets you own (and the better you manage debt), the higher your net worth.

- Foundation for Wealth-Building Strategies: Assets are the backbone of smart, long-term wealth and are more reliable than chasing quick wins.

- Financial Independence: Cash-flowing assets can reduce reliance on your paycheck and help you progress towards financial independence earlier in life.

Make Smart Asset Choices

Lease vs. Buy (Vehicles)

The debate: One interesting debate in owning assets is whether you should lease or buy. Using a car as an example, should you lease it or just buy it outright? The argument for leasing is that you can get the most up-to-date models, technology changes may make some cars obsolete (think the emergence of electric vehicles), and it allows you to try new car brands and models every few years. Although some of these arguments are valid, I just feel the value of owning a car far outweighs the value you would get from leasing.

Key fact to remember: Cars are depreciating assets. Some brands depreciate more slowly and are cheaper to maintain (e.g., Toyota, Honda) than luxury brands.

Simple Example

Let’s break down a scenario to see if leasing a car or buying a car would be better.

- Lease: $300/month × 180 months (15 years) = $54,000 (ignoring down payments, fees).

- Buy: $25,000 new and keep for 15 years. If resale value is $3,000–$5,000 after 15 years, your net cost is ~$20,000–$22,000 before maintenance/repairs/financing.

- Which Option Wins: In this simplified scenario, buying could save you between $32,000–$34,000.

You can also sell the car you bought or give it to a family member, further extending the value. If this were a real-life scenario, you would need to take into consideration maintenance repairs, insurance, and some other costs; however, this simple example shows you how you can build wealth and save money with assets, even in everyday decision-making.

Quick Comparison of Both Options

| Factor | Lease | Buy | Notes |

| Monthly Cost | Usually lower upfront | Varies; can be lower long-term | Buying used can lower the cost |

| Maintenance | Often covered in lease term | On you after the warranty | Reliability matters a lot |

| Flexibility | Easy to change every 2 – 3 years | Keep as long as you want | Buying gives you an asset to sell |

| Total Cost (Assuming 15 yrs.) | Typically higher | Typically lower | Depends on model and usage |

Renting vs. Owning Property

Renting vs. owning property takes this situation one step further, as a property value has two parts: the structure (which wears out) and the land (which can appreciate). Overall returns depend on location, time horizon, improvements, and market conditions

One reason people lean towards renting vs. buying a house is because of capital constraints. This is why being able to save properly is so important. Having good saving habits will provide you with the capital to buy a house. Some may feel it’s daunting to save for a house, and I get that. It took me almost 6 years of savings, but with smart financial habits, those small savings add up over time. With some patience, I was able to buy my first duplex in New York City.

If you want to hear more about my story and inspiration for this blog, you can check it out here. But if you want the quick version, by purchasing a duplex and house hacking (renting one unit and living in the other), I was able to substantially decrease my monthly mortgage expense, which is what makes owning real estate such a valuable asset to anyone looking to grow their wealth.

Which is Better: The Answer Isn’t That Simple

The younger me would say that you should always try to own property as opposed to renting, but in this economic environment, I’m not sure I agree with that anymore. Let’s take a look at some of the pros of both options.

Pros of buying

- Opportunity for cash flow if you rent part/all of it (e.g., duplex).

- You build equity over time.

- Potential appreciation and tax benefits.

Pros of renting

- In some markets, renting is cheaper than owning after taxes, insurance, HOA, and repairs.

- Fewer surprise costs (landlord handles most repairs).

- Flexibility to move; liquidity if you’re saving to invest elsewhere.

Simple example (house hack):

Let’s look at a home-buying example.

- Mortgage payment: $1,500/month.

- Renting out a unit/room for $1,500/month means your housing cost is effectively $0 (before taxes, insurance, vacancies, capital expenditures).

- Over time, rent can help pay down the mortgage. Once the loan is gone, the incoming rent becomes a more passive income stream.

Tips to Build Wealth With Assets at a Young Age

One tip I found to accumulate more assets is to find hobbies that accumulate assets. This is a great way to combine fun with wealth-building strategies at a young age. Instead of only spending on golf or other pricey hobbies, consider asset‑oriented ones with resale value or income potential. Some of these include:

- Sports card or TCG trading

- Sneaker collecting

- Fixing and flipping old cars

- Ebay or garage sale hunting

- Content creation (YouTube, blog, digital products)

All of these hobbies may require you to spend money; however, the important distinction is that you’re not wasting money. You can sell these assets later to recoup some of your initial investment or even make a profit.

The Plan on How to Start Building Wealth With Assets Early

Building wealth isn’t about chasing the next big thing. It’s slow, methodical, and in many ways a boring task. It’s about having the mental discipline to save properly and strategically invest those savings over time, managing both risk and reward. The goal here is financial independence through assets, allowing you to work less and letting your assets work for you. The more valuable assets you own, the stronger your financial foundation becomes. Prioritize cash-flowing investments, appreciating property, and skills or side hustles that generate income. That’s the true engine for long-term wealth. Now it’s your turn. I want you to think about what assets you are building today and how they will grow both in the short term and in the next 10+ years. Below are some steps you can take in the next 30, 60, and 90 days to start growing your assets immediately.

30‑60‑90 Day Asset Plan

30 days

- Build a 3‑bucket budget (Needs/Wants/Investing).

- Set up an automatic monthly investment into a broad, low‑fee index fund.

- List your current assets and liabilities; set a baseline net worth.

60 days

- Price a realistic house hack in your city (actual listings + conservative rent comps).

- Get 3 insurance quotes for your car; prioritize reliability to lower lifetime costs.

- Cut one “want” and redirect savings to investing.

90 days

- Add one skill‑based asset (course, certification, portfolio project).

- Sell unused items; invest the proceeds.

- Set a 12‑month asset acquisition goal ($ amount or % of income).

Ready to start? I know you got this.

Share this post with a friend who’s building wealth too, and drop a comment with the next asset you’re targeting.

Cars are depreciating assets. They have resale value, but typically lose value. Keep costs low and hold reliable models longer.

A diversified, low‑fee index fund is the easiest on‑ramp for most beginners.

Aim for a 3–6 month emergency fund before making illiquid purchases.

No. Renting buys flexibility and reduces the risk of surprise housing costs. In some markets, it’s the better choice while you save/invest.

If you value always-new vehicles, want predictable costs, or have specific business tax considerations (talk to a professional).

2 Comments

Comments are closed.