Walmart OnePay Credit Card: Is it a Banger or a Bust?

The Walmart OnePay CashRewards Credit Card dropped in 2025. Is it a banger or a flop? In this post, we will dive into everything that makes this card special, who it’s for, and who should pass on it, and at the end, I’ll give you a secret strategy for max value by pairing this card with another special one.

TL;DR

- Walmart ended its Capital One partnership and is rolling out two Synchrony-issued cards embedded in the OnePay app in fall 2025.

- New lineup includes: Walmart OnePay credit card (CashRewards Mastercard) for general use and a Walmart Spend Card for in‑store use only.

- Best for Walmart+ loyalists who want up to 5% back at Walmart; pair with a 2% card for non‑Walmart purchases.

- Bottom line: If you shop at Walmart a lot, the Walmart OnePay CashRewards credit card can be a top earner; otherwise, consider broader cash‑back or travel cards.

Get approval ready in under 5 minutes. Check out this Credit Card Approval Checklist you need for your next application.

What Changed and Why It Matters

Walmart and Capital One parted ways back in 2024, and since then, there has been a hole for a solid and reliable card to use for everyday spending. They have since rebuilt their card program with Synchrony and its fintech affiliate OnePay. The new Walmart OnePay credit card portfolio, managed inside the OnePay app, replaces the old Capital One era. For Walmart loyalists (especially Walmart+ members), this shift could mean higher earn rates and a tighter in‑app experience.

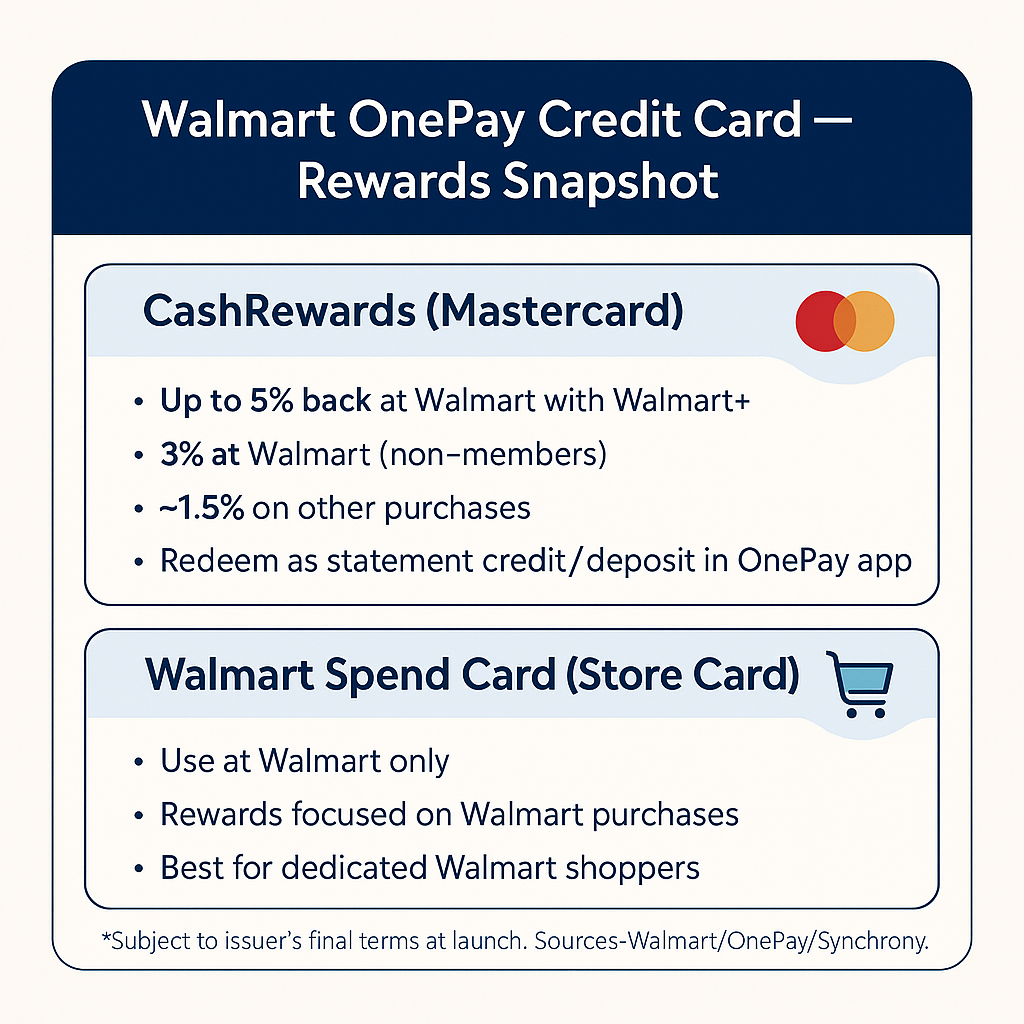

Walmart OnePay Credit Card: Rewards Snapshot (What We Know)

The Walmart OnePay credit card (CashRewards Mastercard) earns 5% back at Walmart for Walmart+ members, 3% for non‑members, and ~1.5% on other purchases. It also comes with a $0 annual fee. If you have Walmart+, this card is perfect for anyone looking to build wealth, as you’ll be getting 5% back on major spend categories like online shopping and groceries. If you don’t get approved for the Walmart CashRewards Card, you’ll likely get offered the Walmart Spend Card (store card). It’s usable only at Walmart and is designed for shoppers who want a simple, Walmart‑first card. If you’re concerned, you’ll get denied. Check out this post where I go through the best credit cards to get for building a better credit score.

Compared to the prior Capital One Walmart Rewards structure, the Walmart OnePay credit card improves the non‑Walmart earn rate to ~1.5% everywhere, but dedicated 2% cards like the Capital One VentureX can still beat it for non‑Walmart spending.

Who the Walmart OnePay Credit Card Is Best For

This card is fantastic for Walmart+ members who do most grocery and general shopping at Walmart and want a simple, high-earning rate there. It’s also valuable for shoppers who prefer cash‑like rewards and easy redemptions inside the OnePay app over travel transfer ecosystems.

Who Should Skip It (and Why)

Anyone seeking a strong catch-all credit card should look elsewhere. A flat 2% cash‑back card will often outperform this card away from Walmart. Additionally, travelers who value transfer partners, lounges, and premium protections should opt for a travel ecosystem instead. Keep reading for a fantastic hack, however, that combines the best of both worlds.

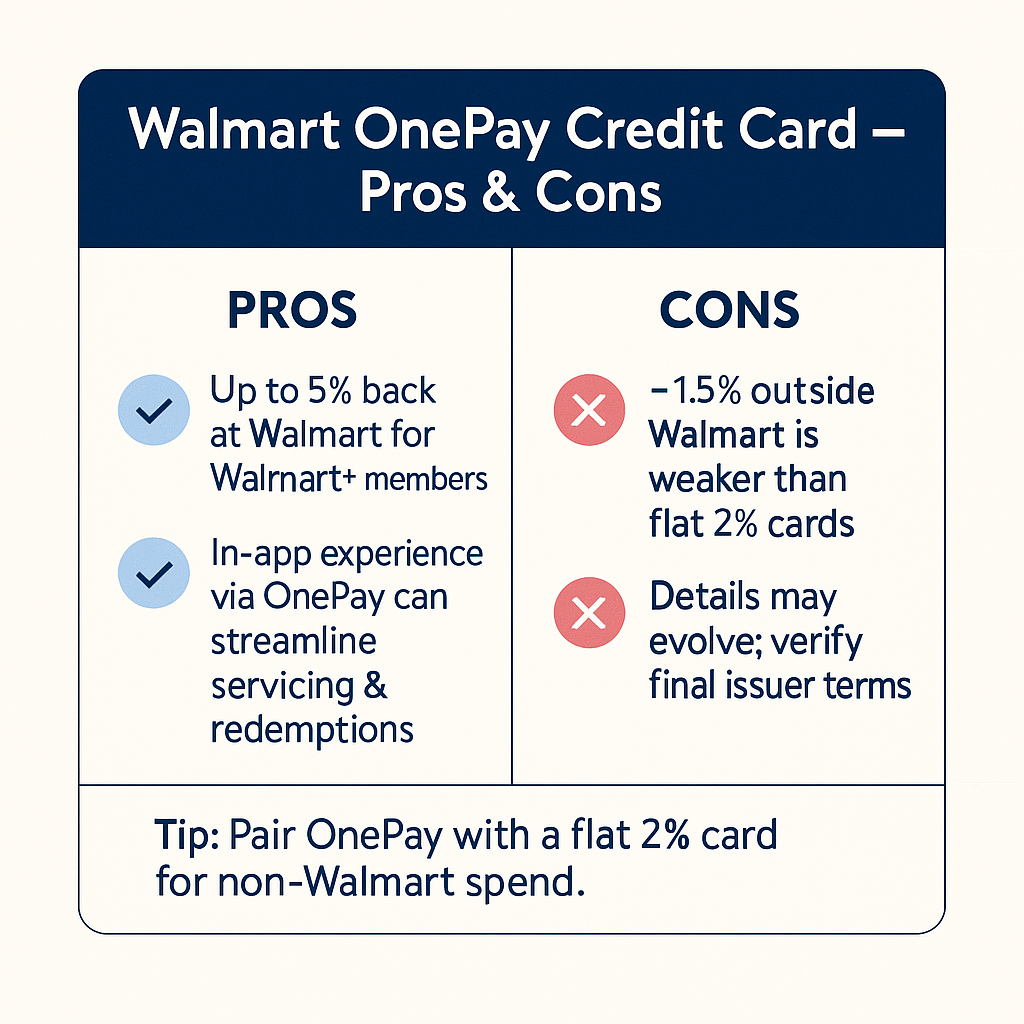

Pros and Cons

Alternative Options that May Be Worth Considering

- Flat‑rate 2% cash‑back cards for non‑Walmart spend – Capital One VentureX (travel) or Citi Double Cash (Cash back)

- 5% rotating or category cards for when Walmart or online shopping is the quarterly category – Chase Freedom Flex (Travel) or DiscoverIt Cash Back (Cash Back)

- Grocery‑centric cards if you rarely shop at Walmart – Capital One Savor Cash Rewards or Amex Gold

If You Have the Capital One Walmart Card

Capital One and Walmart ended their partnership in 2024. You can typically continue to use your existing Capital One account and redeem rewards, but many cardholders are being migrated to Capital One’s core products (for example, Quicksilver 1.5%). Watch your Capital One messages for specifics about your account.

Final Thoughts

If Walmart is your main store and you already have Walmart+, the Walmart OnePay credit card can be your #1 card at Walmart. Pair it with a flat 2% card for non‑Walmart purchases. Pro tip: If you already have the Amex Platinum and use the Walmart Plus credit, you unlock the top earn for no additional spend. Before applying, check out this free Approval Confidence Checklist to improve your odds and put you in the best position to be approved (terms apply). Never carry a balance for rewards. If you need help paying off debt, check this article out on 9 proven strategies to pay off debt with little income.

FAQ

No, the new Walmart OnePay credit card setup supersedes the old structure. Check your Capital One app for current benefits and any migration notices.

Yes, coverage indicates Walmart+ members get the top rate (5%). Non‑members earn less (e.g., 3%). Verify final terms at application.

It’s ok, but there are better options. You should aim for 2% everywhere. Consider a two‑card strategy: a Walmart OnePay credit card for Walmart, and a 2% card for everything else.

Some accounts are being migrated by Capital One; check messages in-app.

Disclosure: This post contains affiliate links. I may get a small commission or points if you use my links. This is not financial advice and is for educational purposes only. The views and opinions in this article and blog or mine alone. For more information, please read my website policies and disclaimers.