Bilt Palladium vs Venture X: Which Catch-All Wins?

The Bilt Palladium launched and the internet lost its mind. Half the creators are calling it the new premium king. The other half are ripping it apart. And honestly, most of those takes are missing the math.

So here’s what we’re doing today: a full Bilt Palladium vs Venture X breakdown, side by side, with real numbers. No hype, no outrage farming. Just two premium catch-all cards, the actual math on what you’re paying and what you’re getting back, and a clear answer on which one wins for most people.

I’ve been tracking both of these cards as part of my 2026 strategy, and after running every scenario I could think of, the answer is clear. But it might not be for the reasons you’d expect.

Key Takeaways:

- With straightforward credits, the Venture X effective annual fee can drop to near $0. Meanwhile, the Palladium’s credits come with calendar windows, portal rules, and expiration dates.

- A dual-earn system on the Palladium creates an effective 3.33x catch-all rate, but only if you hit specific non-housing spend thresholds.

- For 99% of people, the Venture X wins based on simplicity, travel perks, and net value after credits.

- One narrow use case exists for the Palladium: one-card setups where housing points matter more than travel protections.

Bilt Palladium vs Venture X: What Changed with Bilt 2.0

Want to run this math on your spending? Plug in your real numbers and see what each card actually earns you.

Free Calculator →Before we compare these cards, you need to understand what Bilt actually did, because so many people are failing to grasp the fundamental shift here.

The Bilt 1.0 Acquisition Play

Bilt 1.0 was a rent card. That was the whole pitch: earn points on your rent with no fees. It was one of the easiest cards for anyone to recommend. But let’s call it what it was, an acquisition play. As a result, Bilt was hemorrhaging money paying out tens of thousands of points (if not hundreds of thousands) to people who were literally buying two dollars worth of purchases split into four transactions per month.

So why were they willing to do that? Because acquisitions gave them leverage to negotiate with transfer partners and drove interaction on their platform.

How Bilt 2.0 Changed Everything

Bilt 2.0 is a completely different business. These are not rent cards. Instead, they are premium credit cards that happen to offer a housing points component. Bilt doesn’t even allow you to use credit to pay rent anymore, which was the single biggest benefit of 1.0. Where Bilt 1.0 was about acquisitions, Bilt 2.0 is about transaction fees and profitability. They’re expecting people to be outraged and leave. Ultimately, they won’t care, because they achieved their goal: grow a massive user base, then restructure so the only people who stick around are the ones actually spending on the cards.

At their core, these cards are no different than the Amex Gold or Sapphire Preferred. They earn rewards based on everyday spend, and it just so happens that part of those rewards let you redeem extra points (almost like a coupon) on your rent or mortgage.

That context matters for this comparison. Rather than evaluating the Palladium as a rent card, you should evaluate it as a premium catch-all that competes directly with the Venture X.

If you want to see how cards like these fit into your overall wallet strategy, I built a free toolkit that runs the math on any card combination.

Grab the free Rewards & Returns Guide here

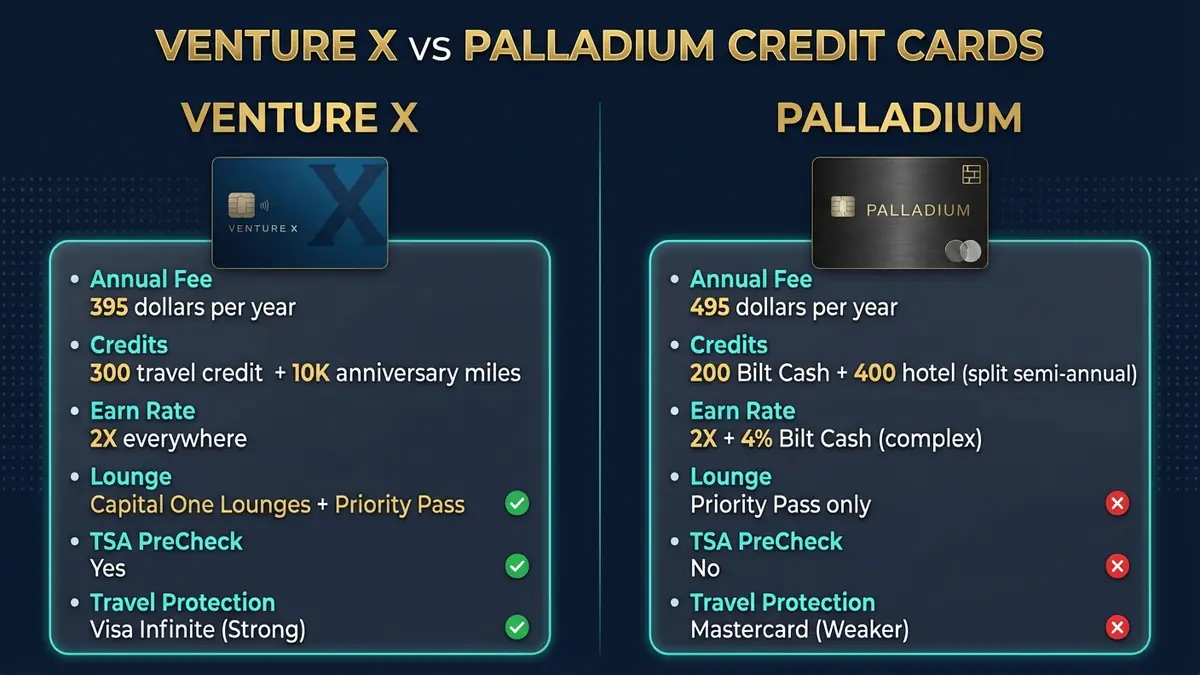

Capital One Venture X: The Simple Premium Catch-All

Most premium cards come loaded with credits that sound great on paper but require a spreadsheet to actually use. However, the Venture X flips that script, and that’s what makes it dangerous.

Annual Fee and Credits

The Capital One Venture X comes with a $395 annual fee and a standard bonus of 75,000 points (as of April 2026).

Here’s how the offset works:

- $300 annual travel credit when you book through Capital One Travel

- 10,000 anniversary miles every year starting year one, worth about $100 at 1 cent per mile

If you actually use both, your effective fee drops to roughly $0. Zero calendar windows, zero minimum stays, and zero expiring coupons.

Earn Structure

A Capital One Venture X review starts and ends with simplicity:

- 2X miles on every purchase. That’s the baseline catch-all rate.

- 10X on hotels and rental cars booked through Capital One Travel

- 5X on flights (and often vacation rentals) through the portal

- 5X on Capital One Entertainment purchases

In other words, it’s 2X everywhere, with bonus multipliers if you use the portal. No dual-currency system, no unlock mechanisms.

Lounge Access and Travel Perks

You get access to Capital One Lounges and Landings plus Priority Pass lounges.

But effective February 1, 2026, two changes hit:

- Authorized users no longer automatically get lounge access. You can add it for $125 per year per cardholder.

- Free guests at Capital One Lounges require $75,000 in annual spend on the account. Otherwise, guests cost extra.

If you’re solo, this changes nothing. On the other hand, if you were using the Venture X as a family lounge hack, the math gets muddier.

The Underrated Perks

These don’t make the headlines but they add real value:

- Price drop protection and price match

- Global Entry / TSA PreCheck credit up to $120

- No foreign transaction fees

- Primary auto rental collision damage coverage (huge if you’re in a state like New York where so many cards dropped this)

- Visa Infinite travel and trip protections

The Venture X is the closest thing to a “set it and forget it” premium card in 2026. The credits are easy to use, the earn rate is clean, and the travel protections are legitimately strong. Is the Venture X worth it? For most people building a premium wallet, yes, and it’s not even close.

Additionally, if you’re looking for a strong no-annual-fee card with transfer partners to pair alongside a premium card, check out the Wells Fargo Autograph. It’s one of the best free cards in the game right now.

Bilt Palladium Review: The Complex Premium Play

Now here’s the real question: can the Bilt Palladium beat this as a catch-all?

With a $495 annual fee and a 50,000 point signup bonus (as of April 2026), the Palladium positions itself as a premium competitor. If you want the full deep-dive on the card’s benefits and point valuations, The Points Guy has a solid review. But here’s my take on how it actually stacks up against the Venture X.

The credit structure is where things get complicated:

Credits Breakdown

$200 in Bilt Cash annually:

- Bilt Cash is essentially coupons redeemable for specific things inside Bilt’s ecosystem: Lyft rides, unlocking points on your mortgage or rent, and other platform-specific redemptions.

- Credited on card approval, then hits January 1 each year after that.

- Expires after 1 year, but you can carry over up to $100 to the next year.

$400 Bilt Travel Hotel Credit annually:

- Split into two windows: $200 January through June and $200 July through December

- Only valid for hotel bookings through the Bilt Travel Portal

- Requires a minimum 2-night stay to qualify

- Credits can take 8 to 10 weeks to show as statement credits

This is exactly why people call this card confusing. Unlike the Venture X, you’re juggling calendar windows, portal rules, minimum stay requirements, and expiration dates.

Earn Structure

Here’s where the Palladium gets interesting, and also where it gets confusing:

- 2X Bilt Points on everyday purchases (not rent or mortgage)

- Plus 4% back in Bilt Cash on those same purchases

Essentially, it’s a dual-earn system. Every swipe gives you points AND Bilt Cash. No other major premium card works this way, which is part of why people struggle to evaluate Bilt points value accurately.

The Housing Points Unlock (and Why It’s Convoluted)

This is the big Bilt 2.0 change: points on housing aren’t automatic anymore.

You can earn up to 1X on rent and mortgage, but it’s unlocked using Bilt Cash through a tiered structure. Some people say you need to spend 75% of your housing payment on non-housing purchases to unlock the full 1X. That’s not exactly right. In reality, you need that spend level to unlock the full 1X, but you can still unlock partial points on your mortgage at lower spend levels.

Here’s the key formula: every $30 in Bilt Cash earned unlocks 1,000 Bilt Points on a rent or mortgage payment, up to your housing payment amount.

I built a free credit card strategy tracker that handles exactly this kind of math. Get it here

Lounge Access

With the Palladium you get Priority Pass access for you and up to two guests. Additional guests cost $35 per visit. Authorized users run $95 per year.

However, there’s no Capital One Lounge access, no TSA PreCheck credit, and the Mastercard travel protections are objectively worse than what you get on the Venture X’s Visa Infinite network.

The Math: Palladium Effective Earn Rate Explained

Most people I work with find $300–$800/year in missed rewards from one wrong card or one misassigned category. I map your real spending and build a custom plan in a 30-minute call.

Not financial advice. Results vary by individual spend.

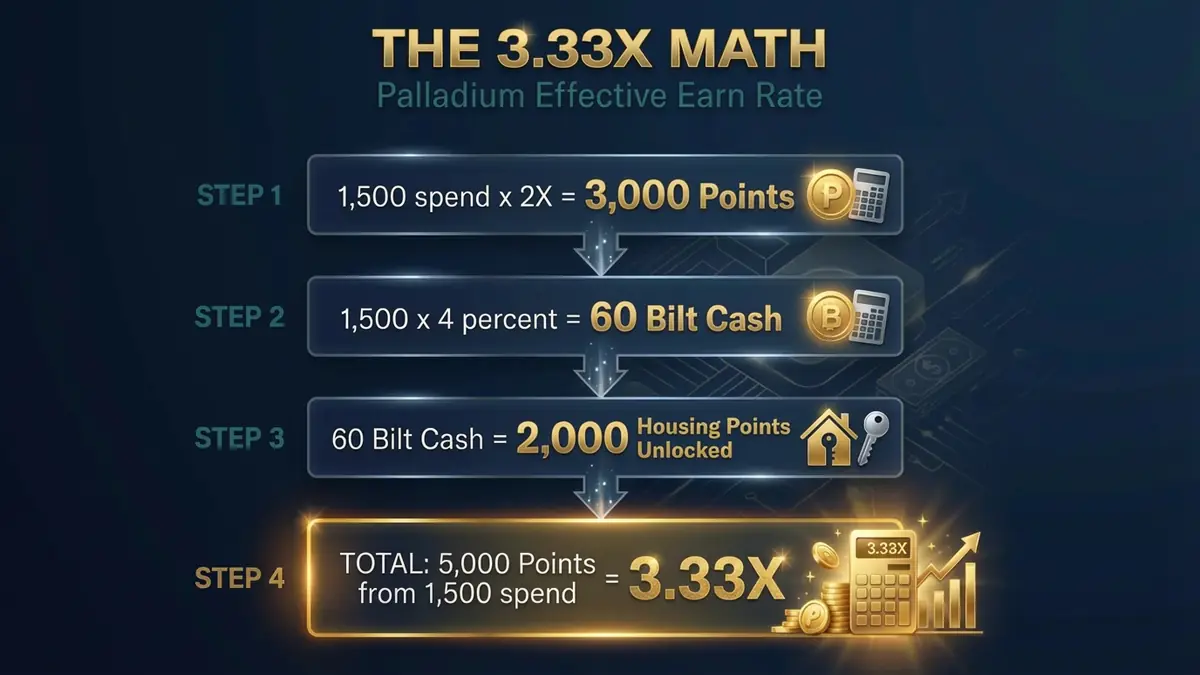

You’ve been told the Palladium is a 2X catch-all. That’s technically true, but it undersells what the card actually does when you factor in the Bilt Cash component. So let me walk through the real numbers.

Running the Numbers

Scenario: $2,000 mortgage, $1,500 in non-housing spend per month

First, non-housing spend earns 2X Bilt Points.

$1,500 x 2 = 3,000 Bilt Points

That same spend also earns 4% Bilt Cash.

$1,500 x 0.04 = $60 in Bilt Cash

Next, redeem that Bilt Cash to unlock housing points.

$60 Bilt Cash = 2,000 Bilt Points unlocked on your mortgage

Finally, add it all up for total monthly points from $1,500 in actual card spend.

3,000 + 2,000 = 5,000 Bilt Points

5,000 points from $1,500 in non-housing spend = an effective 3.33X catch-all rate. But only up to 75% of your housing payment. After that threshold, the value shifts depending on how else you use Bilt Cash.

That 3.33X rate assumes $2,000 in housing and $1,500 in non-housing spend, yours will be different. Most people I work with are leaving $300-$800/year on the table from one wrong card, one misassigned category, or one annual fee that doesn’t pencil out. I run 1:1 Spend Audits: I map your real spend, check your issuer rules, and hand you a written optimization plan you can execute the same week. Book a Spend Audit ($97)

The Reality Check

That 3.33X rate is real, but it comes with asterisks. You need consistent non-housing spend to fuel the Bilt Cash engine and you need to actively redeem that cash for housing point unlocks.

Compare that to the Venture X: 2X on everything, with zero unlocking required, zero calendar windows to track, and zero secondary currencies to manage.

The Ecosystem Problem

Right now, one of the main problems I have with the Palladium is that Bilt’s ecosystem isn’t developed enough to justify its own currency. For example, I live in New York and have one Bilt dining program within 10 miles of me, and it’s a coffee shop. They’re trying to turn Bilt Cash into its own rewards ecosystem, and it’s not a strong play. Until that ecosystem matures, the non-housing redemption options for Bilt Cash are limited.

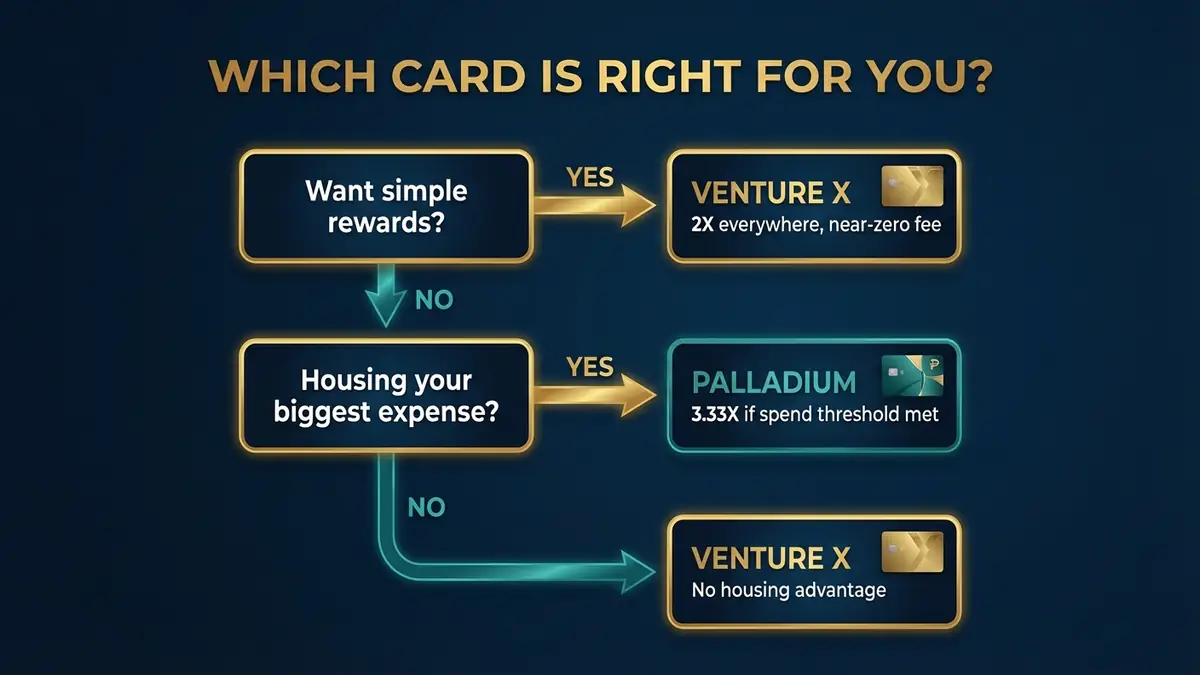

Best For / Not For

Who Should Get the Venture X

Best for:

- Travelers who want a premium catch-all with near-zero effective annual fee

- People who value simple, predictable earning (2X on everything, no second currency)

- Frequent flyers who use Capital One Lounges or Priority Pass regularly

- Cardholders who want strong travel protections, including primary rental car coverage and TSA PreCheck

Not for:

- People who need housing points as a core part of their strategy

- Families relying on free guest lounge access without hitting the $75,000 spend threshold

- Cardholders carrying credit card debt. Pay that off first.

Who Should Get the Palladium

Best for:

- One-card strategists who want the highest possible effective earn rate and are willing to manage the complexity

- Renters or homeowners with high housing payments ($2,000+) who will consistently spend enough to unlock the full 1X

- Points enthusiasts who value Bilt’s transfer partners (Hyatt, Alaska, Japan Airlines) over Capital One’s partner list

- Year-one testers: the 50,000 SUB makes year one positive value even if you cancel after

Not for:

- Travelers who want a straightforward premium card (no TSA PreCheck, weaker lounge access, worse travel protections)

- People who won’t hit consistent non-housing spend to fuel the Bilt Cash system

- Those frustrated by calendar-window credits, portal-only bookings, and expiration dates

- Cardholders carrying credit card debt. Pay that off first.

Capital One’s Venture X wins this comparison for 99% of people. Its effective fee is near zero, the earn rate is clean, travel perks are strong, and you don’t need a spreadsheet to figure out what you’re getting. Meanwhile, the Palladium has a narrow lane for one-card maximizers willing to manage the complexity, but it’s advertised as a premium travel card that doesn’t include TSA PreCheck, has poor lounge access, an extremely complex earn structure, and hotel credits that try to compete with FHR but fall substantially short.

Venture X Rating: 4.2/5 — Premium simplicity done right, with the 2026 lounge changes as the only real ding.

Palladium Rating: 3.8/5 — Interesting math on the 3.33X earn rate, but the execution is too complex and travel perks are too thin for a $495 card.

Final Thoughts

There’s no question in my mind: the Venture X is the better premium catch-all for the vast majority of people reading this. That doesn’t mean the Palladium has zero market. If you want a one-card setup with decent multipliers and housing is your biggest expense, the Palladium could make sense. And the SUB makes year one positive value, so there’s no harm in testing it.

But I won’t be going with the Palladium myself in 2026. And I’ll be hoping Bilt gives this card a serious refresh soon, because the bones are there. The execution just isn’t.

I went deeper on this with the full math and a bit of a rant in the video. Worth watching if you want to hear me really get into it.

Let me know your thoughts. Which card are you going with, and why?

If you want the full spreadsheet system I use to track stacks like this: Rewards & Returns Guide

Bilt Palladium vs Venture X FAQs

Is the Bilt Palladium worth the $495 annual fee?

For most people, no. The $600 in annual credits sounds good on paper, but $200 is in Bilt Cash (limited redemption options) and $400 is split into semi-annual hotel credits with 2-night minimums and portal-only bookings. Compare that to the Venture X’s simple $300 travel credit plus 10,000 anniversary miles. However, the Palladium’s year-one SUB of 50,000 points does make the first year positive value, so testing it carries low risk.

What is the effective earn rate on the Bilt Palladium?

It earns 2X Bilt Points plus 4% Bilt Cash on non-housing purchases. When you redeem that Bilt Cash to unlock housing points (every $30 unlocks 1,000 points), the effective rate on non-housing spend works out to roughly 3.33X, assuming your non-housing spend is at least 75% of your monthly housing payment.

Can you still pay rent with the Bilt Palladium?

You can earn points on rent and mortgage payments, but not by paying with credit directly (that was a Bilt 1.0 feature). Under Bilt 2.0, housing points are unlocked by spending Bilt Cash earned from non-housing purchases. Basically, the more you spend outside of housing, the more housing points you unlock.

Is the Capital One Venture X still worth it in 2026?

Yes. Even with the February 2026 lounge access changes (no more free authorized user access, guest access requires $75,000 annual spend), its core value remains strong: $300 travel credit, 10,000 anniversary miles, 2X everywhere, and solid Visa Infinite travel protections. For solo travelers, the effective annual fee is still close to zero.

Which card has better transfer partners, Bilt or Capital One?

Bilt generally has more valuable transfer partners, including Hyatt, Alaska Airlines, and Japan Airlines. In contrast, Capital One’s partner list is solid but more focused on mainstream carriers. If transfer partner quality is your top priority and you’re willing to manage the complexity, Bilt has an edge here. For everyone else, Capital One’s simpler earning and decent partners are more than enough.

Bilt Palladium

2x everyday, 4% Bilt Cash flexible. $400/yr hotel credit, $200 Bilt Cash, Priority Pass. Up to 1.25x housing.

$495/yr

American Express Gold Card

4x dining and US supermarkets. $10/mo Uber Cash, $10/mo dining credit, $7/mo Dunkin', $100 Resy credit/yr.

$325/yrTerms apply. Some links are affiliate links. I only recommend products I personally use or genuinely believe will help you. Pay your balance in full.

Some links in this article are affiliate links. I only recommend products I personally use or genuinely believe will help you. Terms apply. Pay your balance in full. Applying for a credit card results in a hard inquiry. I’m not a financial advisor or CPA. This is personal experience and opinion.