Chase Sapphire Preferred Downgrade: Why I Kept the Ink Preferred Instead

I just booked a trip on my Chase Sapphire Preferred. Used the $50 hotel credit. It worked fine.

But I’m still planning to downgrade it anyway.

If you’re on the fence about the same move, stick with me. I’m going to run the actual numbers and show you exactly how I’m handling the downgrade.

Key Takeaways:

- The Ink Business Preferred earns 3X on travel vs. the CSP’s 2X. On $5,000 in annual travel spend, that gap is worth roughly $100 per year when you value UR points at 2 cents each via transfer partners.

- The Freedom Flex already earns 3X on dining at zero annual fee. That makes the CSP’s strongest multiplier redundant for anyone already holding a Freedom Flex.

- Paying your monthly phone bill with the Ink Business Preferred unlocks up to $1,000 in cell phone protection per claim. One claim covers more than 10 years of annual fees.

- The cleanest downgrade path: call Chase and ask about a retention offer, then drop the CSP to the OG Chase Freedom, then add the Freedom Flex for the welcome bonus and dining coverage.

- Chase Sapphire Preferred Downgrade: What the Math Actually Says

- Where the Ink Business Preferred Has the Edge on Travel

- The Dining Redundancy Problem

- Cell Phone Protection: The Benefit Nobody Calculates

- My Actual Chase Sapphire Preferred Downgrade Plan

- Who the Ink Business Preferred Is and Isn’t For

- Final Thoughts

- Chase Sapphire Preferred Downgrade FAQs

| Chase Sapphire Preferred | Chase Ink Business Preferred | |

|---|---|---|

| Annual fee | $95/yr | $95/yr |

| Welcome bonus | 75K UR · $5K/3mo | 100K UR · $8K/3mo |

| Top earn rates | Chase Travel Portal 5x · Dining 3x · Streaming 3x | Travel/Ads/Ship 3x |

| Top partners | Hyatt · United · Southwest See all → | Hyatt · United · Southwest See all → |

| Card network | Visa Signature | Visa Signature |

| Foreign tx fee | 0% | 0% |

| Best for | Dining/grocery-heavy spenders, no business income, clean UR entry point | Travel-heavy spenders with business income: 50% more points per travel dollar |

| Not for | Travel-focused spenders who already hold a Freedom Flex for dining | W-2 only with no qualifying business activity |

| Apply Now → | Apply Now → |

Annual fee

Welcome bonus

Top earn rates

Top partners

Card network

Foreign tx fee

Best for

Not for

CHASE SAPPHIRE PREFERRED

Apply Now →CHASE INK BUSINESS PREFERRED

Apply Now →Terms apply. Some links are affiliate links. Credit card comparisons assume you pay your balance in full every month. Offers shown reflect what was current at publication date.

Chase Sapphire Preferred Downgrade: What the Math Actually Says

Want to run this math on your spending? Plug in your real numbers and see what each card actually earns you.

Free Calculator →Same $95 annual fee. Same Ultimate Rewards currency. Both cards also transfer points at the same 1:1 ratio.

On paper, the Ink Business Preferred and the Chase Sapphire Preferred look almost identical. In practice, they operate in completely different categories.

The Ink Business Preferred at a Glance

The Ink Business Preferred is sitting at a 100,000-point welcome bonus right now after $8,000 in spend over three months. Always check Chase’s site before you apply though. They move these offers around.

Earn rates: 3X on broad travel, 3X on shipping, internet, cable, phone services, and advertising up to $150,000 in combined spend per year, and 5X through the Chase Travel portal. When you pay your phone bill with it, you also get up to $1,000 in cell phone protection per claim.

That last one gets buried. But it shouldn’t.

And because it’s a business card, it doesn’t hit your 5/24 count. If you’re still building out your personal card stack, that matters a lot.

The Chase Sapphire Preferred at a Glance

The Chase Sapphire Preferred comes in at the same $95 annual fee, currently sitting at a 75,000-point bonus after $5,000 in spend over three months.

It earns 3X on dining, online groceries from eligible stores (not Walmart, Target, or warehouse clubs), and select streaming. Travel outside the portal earns 2X. Portal bookings get 5X. There’s also a $50 annual hotel credit when you book through Chase Travel.

On paper, it looks competitive. That’s kind of the whole problem.

Both cards hit the same transfer partners: United, Hyatt, Southwest, Air Canada Aeroplan. Same 1:1 ratio. That part is a wash.

If you want to run this against your own numbers, the Credit Card ROI Calculator in my Rewards & Returns Guide is built for exactly this.

Grab the free Rewards & Returns Toolkit →

Check the video above if you want to see this live.

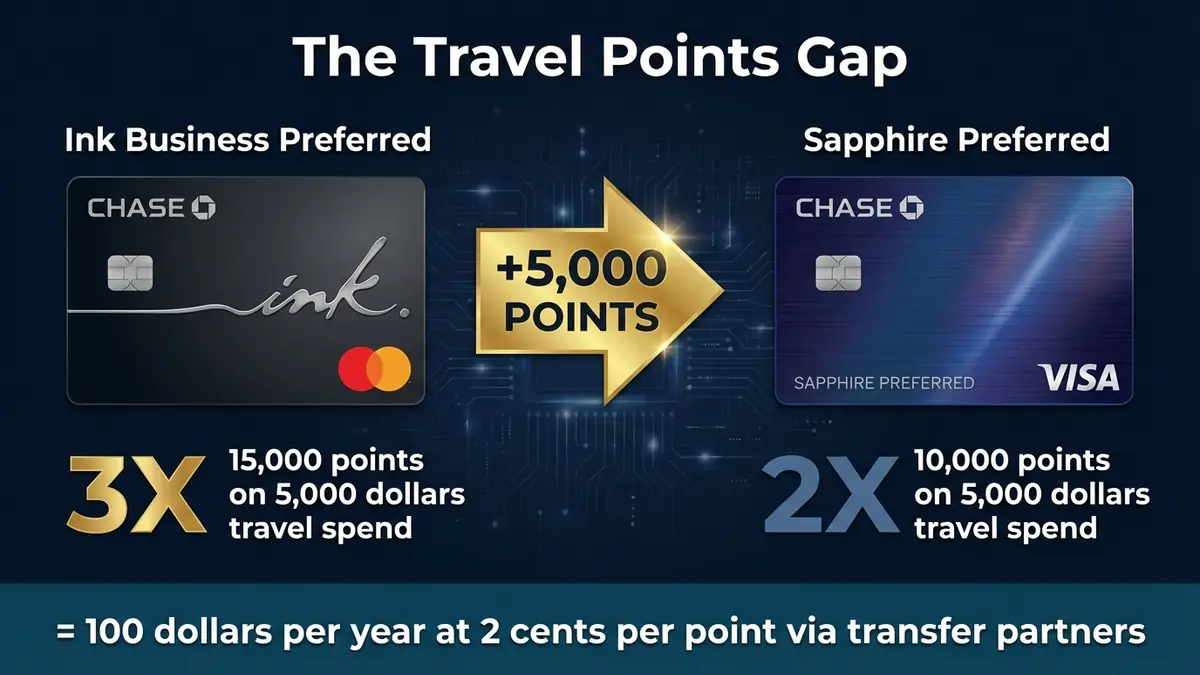

Where the Ink Business Preferred Has the Edge

This is the main reason I’m keeping the IBP. One multiplier gap that most people completely miss.

The IBP earns 3X on broad travel. Not portal travel. Broad travel: flights, hotels, rental cars, trains, metro cards, tolls, and parking. All of it at 3X.

The Sapphire Preferred earns 2X on travel outside the portal.

That one-point difference is actually a 50% increase in points earned per dollar. On $5,000 in annual travel spend, the math breaks down like this:

- Ink Business Preferred: $5,000 × 3X = 15,000 UR points

- Chase Sapphire Preferred: $5,000 × 2X = 10,000 UR points

- Difference: 5,000 points per year

At 2 cents per point via transfer partners, that gap is worth $100 annually. That valuation aligns with The Points Guy’s current UR estimate and is actually on the conservative end for Hyatt redemptions. And $5,000 in travel spend is a reasonable assumption for anyone in a metro area with commuting costs, tolls, and one or two trips per year.

$5,000 in annual travel spend: IBP earns 15,000 UR vs. CSP’s 10,000 UR. At 2¢/point via transfer partners, that’s a $100 annual difference from the travel multiplier alone.

In fact, no other Chase card at the $95 price point offers broad 3X on travel. The next option is the Sapphire Reserve at $795 per year. For anyone who wants elevated travel multipliers inside the Chase ecosystem without stepping up to the Reserve, the Ink Business Preferred is the only move.

The Dining Redundancy Problem

Now, to be fair, the CSP’s strongest category is 3X on dining. That’s genuinely good.

But here’s the problem. You can get that exact multiplier on a free card.

The Chase Freedom Flex earns 3X on dining and drugstores with no annual fee. When you pair it with any Ultimate Rewards card, that cash back converts into fully transferable UR points. So if you already hold the Freedom Flex alongside the Ink Business Preferred, you’re covering the dining category at zero additional cost.

That makes the CSP’s 3X dining redundant. You’re effectively paying $95 per year for a multiplier you already have.

The CSP made a lot more sense before the Freedom Flex was this capable. Today, anyone building a Chase stack can cover dining for free. The Sapphire Preferred no longer has a clear lane at $95, and that’s the honest reason to execute the downgrade.

One exception does apply here: 3X on online groceries from eligible stores. Chase doesn’t have a free card that covers online groceries yet. So if online grocery shopping is a meaningful part of your monthly spend, the CSP still has a specific use case. For most people, however, it’s not enough to justify the fee on its own.

The 3X on select streaming services is similarly marginal. Most people spend $15 to $25 per month on streaming. The points difference across that category is minimal.

Free Credit Card Strategy Tools

Get the ROI Calculator, Points Toolkit, and more. I’ll send them straight to your inbox.

Cell Phone Protection: The Benefit Nobody Calculates

Most people skip past this one entirely. That’s a real mistake, though.

When you pay your phone bill with the IBP, you earn 3X on that spend. You also automatically qualify for cell phone protection of up to $1,000 per claim for theft or damage, with a $100 deductible.

In fact, phone repairs and replacements have gotten expensive. A screen repair on a flagship phone can easily run $400 to $600. A full replacement clears $1,000 for many devices.

Here’s what most people miss: one claim pays for more than a decade of the card. That’s not a stretch. That’s a realistic scenario for anyone who has ever cracked a screen or had a phone stolen.

The Sapphire Preferred doesn’t offer this benefit. There’s simply no equivalent protection built into any of its spend categories. For anyone paying their own phone bill each month, which is essentially everyone, this protection is real value that nobody actually factors in.

One thing: you have to charge your full phone bill to the card each month. Partial payments don’t count.

My Actual Chase Sapphire Preferred Downgrade Plan

Most people I work with find $300–$800/year in missed rewards from one wrong card or one misassigned category. I map your real spending and build a custom plan in a 30-minute call.

Not financial advice. Results vary by individual spend.

So here’s exactly what I’m doing.

My CSP annual fee is due this month. The first move is calling Chase and asking about a retention offer. The odds of getting anything meaningful on a Preferred card are low, but it takes three minutes and costs nothing to ask. If they offer 10,000 bonus points to keep the card, that’s worth running through your own math before deciding.

When they say no, I’m requesting a product change to the OG Chase Freedom. Not the Freedom Unlimited. The original Freedom. The OG gives me permanent 5X rotating categories, up to $1,500 per quarter. That card doesn’t take new applicants anymore, so the only way to keep it is to hold it. Downgrading keeps the credit line open, protects my history, and my UR points stay intact.

After that, my next move is applying for the Chase Freedom Flex. That card comes with a 20,000 to 30,000 point welcome bonus, and it restores 3X on dining and drugstores back into my wallet alongside the 5X rotating categories.

The Final Chase Stack

After the full transition, my setup looks like this:

- Dining: 3X on Freedom Flex, $0 annual fee

- Travel: 3X on Ink Business Preferred, $95 annual fee

- Drugstores: 3X on Freedom Flex, $0 annual fee

- Internet, cable, and phones: 3X on IBP with cell phone protection included

- Office supplies: 5X on Ink Cash (check out the Ink Cash vs Ink Unlimited breakdown if you haven’t looked at that card yet)

- Rotating categories: 5X up to $1,500 per quarter on OG Freedom, plus another $1,500 per quarter on Freedom Flex

Ultimately, one $95 card carries the travel and phone categories. Everything else is covered for free.

If you want someone to map this kind of transition against your actual spend, that’s exactly what a Spend Audit covers.

Who the Ink Business Preferred Is and Isn’t For

Neither of these cards is for anyone carrying credit card debt. Pay that off first. Rewards cards only pencil out when you pay the balance in full each month. The interest charges on any unpaid balance will wipe out every point you earn.

The Ink Business Preferred Is Best For:

- Anyone with qualifying business income: freelancing, an LLC, content creation, reselling, or any consistent side income

- Travel-heavy spenders who book direct, not primarily through a portal

- People who want to preserve personal 5/24 slots while still adding a high-value UR card

- Side hustlers or founders looking for a large welcome bonus on a $95 card

- Anyone who pays their own cell phone bill and wants repair and replacement coverage without a separate insurance policy

You can apply with a sole proprietorship, and you don’t need an established business. Consistent freelance income, content creation, or reselling activity all qualify.

The Ink Business Preferred Is Not For:

- W-2 employees with no qualifying business activity. Do not apply without a legitimate use case.

- Cardholders whose spend is concentrated in dining and online groceries with minimal travel

- Anyone who cannot reach the $8,000 spend requirement organically in three months. Do not manufacture spend to chase a bonus.

- People who primarily book through the Chase Travel portal for the 5X rate. Both cards offer 5X through the portal, so that advantage does not differentiate them.

When the Sapphire Preferred Still Makes Sense:

The Chase Sapphire Preferred still makes sense in a few situations. No qualifying business income? It’s your only shot at UR transfer access at the $95 tier. Heavy dining and online grocery spend with minimal travel? The CSP’s earn structure fits that better. Just getting started and want one solid card before building a full stack? It’s still a clean entry point into Chase.

For anyone considering their first business card, I covered the top business credit cards for startups with a full comparison if you want a broader look at the options. The full Credit Card Reviews library has every head-to-head I’ve run.

Final Thoughts

Same $95. Same Ultimate Rewards ecosystem. The difference comes down to where your spend actually lands.

For travel-heavy spenders with qualifying business income, the IBP wins clearly: 50% more points per travel dollar, cell phone protection that covers itself in one claim, and it doesn’t touch your 5/24. At $95, the Ink Business Preferred is the best chase card for travel points in this tier.

For anyone without business income, or someone whose spend is heavy on dining and online groceries, the CSP still has a case. There’s no universal answer. It comes down to where your money actually goes each month.

Run the numbers on your own spend, because that’s where the real answer lives.

If you want the free tracker I use to do exactly this: Rewards & Returns Toolkit →

Drop your current Chase setup in the comments. Are you team Ink or team Sapphire? I want to see what everyone’s running.

Chase Sapphire Preferred Downgrade FAQs

What can I downgrade the Chase Sapphire Preferred to?

You can downgrade the CSP to the Chase Freedom Flex, Chase Freedom Unlimited, or the OG Chase Freedom (if you already hold it). Each option keeps your credit line open and preserves your UR points at no annual fee. You need to have held the card for at least 12 months before requesting a product change. Call the number on the back of your card to initiate the downgrade.

Can I downgrade the Chase Sapphire Preferred directly to the Ink Business Preferred?

No. You cannot switch between personal and business cards through a product change. The CSP downgrade options are limited to personal no-fee Chase cards. The Ink Business Preferred requires a separate application, and it does not add to your 5/24 count when approved.

Will I lose my Chase Ultimate Rewards points when I downgrade the Sapphire Preferred?

No. Your points stay intact when you downgrade to the Freedom, Freedom Flex, or Freedom Unlimited. However, you will lose the ability to transfer points to airline and hotel partners unless you continue holding another UR-transferable card. If you have the Ink Business Preferred in your wallet, that card keeps your transfer access fully active.

Is the Chase Ink Business Preferred better than the Sapphire Preferred for travel?

For most travel-heavy spenders, yes. The IBP earns 3X on broad travel versus the CSP’s 2X outside the portal. On $5,000 in annual travel spend, that gap produces an extra 5,000 UR points, worth roughly $100 per year at 2 cents per point via transfer partners. No other Chase card at $95 matches the IBP’s travel earn rate.

How do I trigger the Chase Sapphire Preferred $50 hotel credit?

Book a hotel through the Chase Travel portal using your Sapphire Preferred. At least a portion of the charge must be billed to the card directly, meaning a pure points booking will not trigger the credit. The $50 statement credit typically posts within one to two billing cycles after the booking date.

Chase Sapphire Preferred

Best mid-tier travel card for beginners. Transfer to Hyatt, United, Southwest.

$95/yr

Chase Freedom Unlimited

5% Chase Travel, 3% dining and drugstores, 1.5% everything else.

$0/yr

Chase Freedom Flex

Rotating 5% quarterly categories, 5% Chase Travel, 3% dining and drugstores.

$0/yrTerms apply. Some links are affiliate links. I only recommend products I personally use or genuinely believe will help you. Pay your balance in full.

Some links in this post are affiliate links. I only recommend products I personally use or genuinely believe will help you. Terms apply. Always pay your balance in full each month. Applying for a credit card results in a hard inquiry on your credit report. Not for anyone currently carrying credit card debt, pay that off first before adding a rewards card to the mix.

Join the discussion

Prompt

What's your experience with this card or strategy? Share your numbers.

Be the first to share your numbers

Real datapoints from the comments make this thread more useful than another review post.

Leave a comment