How to Improve Your Credit Score (11 Strategies)

Most advice on how to improve your credit score boils down to “pay your bills on time.” That’s not wrong. But it’s like telling someone who wants to get stronger to “just go to the gym.” Technically true, completely useless without a real plan.

Your credit score controls the interest rate on your mortgage, your car loan, your next credit card approval, and in some cases whether you even get an apartment. A 50-point difference between a 700 and a 750 can save you tens of thousands of dollars over the life of a mortgage. So the question isn’t whether your score matters. The question is which specific actions actually move the needle, and how fast.

That’s what this guide covers. Instead of vague advice or recycled tips from 2019, these are 11 strategies ranked by how much impact they actually have on your score, with the math to back it up.

Key Takeaways:

- Dropping your credit utilization below 10% is the single fastest way to boost your score, often adding 20-50 points in one billing cycle

- Payment history accounts for 35% of your FICO score, making on-time payments the most important long-term factor

- Authorized user accounts, credit limit increases, and statement date timing are free moves most people never use

- Building an 800+ score is a long game, but scores in the 670-740 range can improve significantly within 30-90 days

What Is a Good Credit Score?

Want to run this math on your spending? Plug in your real numbers and see what each card actually earns you.

Free Calculator →Before running through the strategies, you need to know where you stand and where you’re trying to go. Here’s how FICO breaks down the ranges (as of April 2026):

- Exceptional (800-850): You qualify for the best rates on everything. This is the top tier.

- Very Good (740-799): Most premium credit cards and competitive loan rates are available here.

- Good (670-739): You’ll qualify for most products, but not always at the best rates.

- Fair (580-669): Options get limited. Interest rates jump significantly.

- Poor (300-579): Rebuilding territory. Secured cards and credit-builder loans are the path forward.

Here’s the thing most people don’t realize: the difference between a 670 and a 740 on a 30-year mortgage at average 2026 rates can mean $40,000+ in extra interest over the life of the loan. That’s real money sitting on the table.

FICO’s own loan savings calculator lets you plug in your score and see exactly how much you’d save. Run the numbers for your situation.

Grab the free Rewards & Returns Toolkit if you want tools to track your credit card strategy as your score improves.

How Is Your Credit Score Calculated?

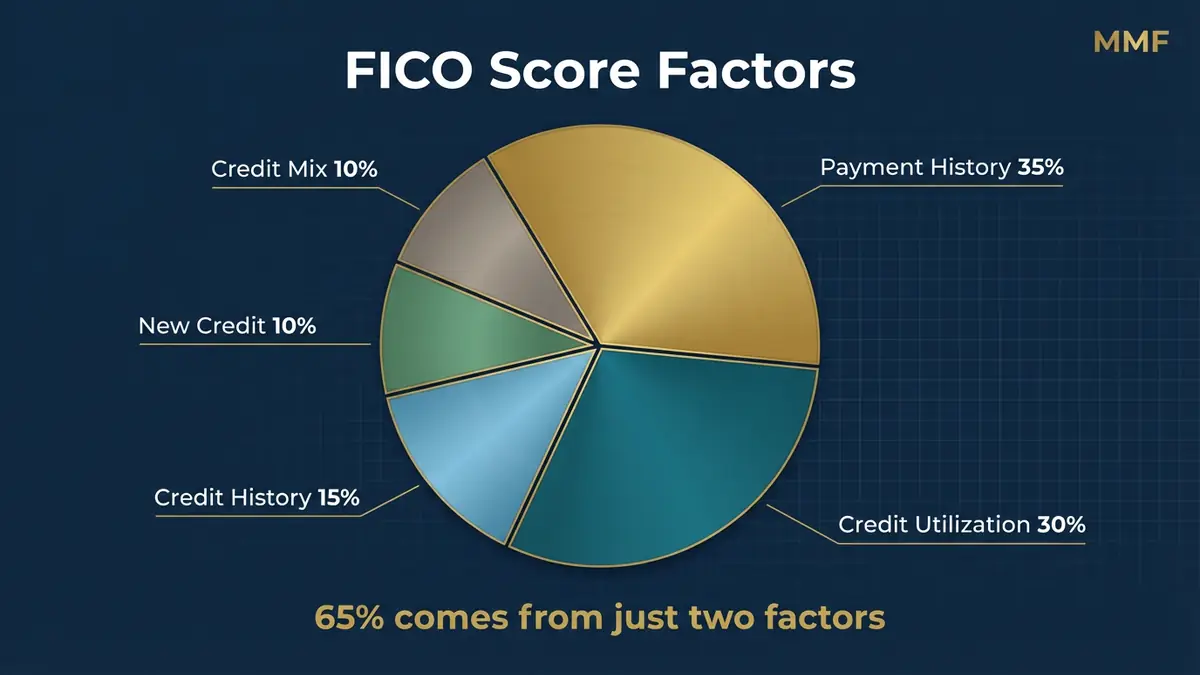

Understanding how your credit score is calculated is the first step to knowing which levers to pull. Your FICO score breaks down into five weighted categories:

The Five FICO Score Factors

Payment History: 35%

Whether you pay on time. Late payments, collections, and bankruptcies live here. This is the single biggest chunk of your score.

Credit Utilization: 30%

How much of your available credit you’re using. If you have $10,000 in total credit limits and carry $3,000 in balances, your utilization is 30%. Lower is better.

Length of Credit History: 15%

The average age of your accounts plus the age of your oldest account. This is why closing old cards can hurt you.

New Credit: 10%

Recent hard inquiries and newly opened accounts. Each hard pull typically drops your score by 2-5 points temporarily.

Credit Mix: 10%

Having different types of credit (credit cards, auto loans, mortgage, student loans) shows lenders you can handle various debt types.

Most “improve your credit score” guides treat all five factors equally. They’re not. Payment history and utilization combine for 65% of your score. If you only focus on two things, focus on those two. Everything else is fine-tuning.

The first two factors, payment history and utilization, account for 65% of your entire score. That’s where the biggest gains come from, and that’s where we’re starting.

11 Strategies to Improve Your Credit Score

These strategies are ordered by impact. The first few can move your score within a single billing cycle. The later ones are longer plays that compound over time.

1. Drop Your Credit Utilization Below 10%

This is the single fastest way to increase your credit score fast. Unlike a late payment that haunts your report for seven years, utilization only reflects your current balances. Pay down your cards, and your score can jump as soon as the new balance reports to the bureaus.

The math is simple. Say you have two credit cards with a combined $20,000 limit and you’re carrying $6,000 in balances. That’s 30% utilization. According to Experian, the highest-scoring consumers typically use less than 7% of their available credit.

As a result, paying that $6,000 down to $1,400 (7% utilization) could produce a 20-50 point increase on your next credit report update. That’s not hypothetical. That’s how the scoring model works.

$20,000 credit limit x 7% target = $1,400 max balance across all cards. If you’re at $6,000, paying down $4,600 could add 20-50 points in one billing cycle.

2. Pay Your Bills On Time, Every Time

Payment history is 35% of your score. One missed payment can drop your score by 80-100 points depending on where you started, and it stays on your credit report for seven years.

Fortunately, the fix is boring but effective: set up autopay for at least the minimum payment on every account. Not just credit cards. Mortgage, car loan, student loans, even your phone bill if it reports to the bureaus.

Here’s the priority order for payment timing:

- First, set up autopay for minimum payments on everything (this is your safety net)

- Then pay the full statement balance before the due date on credit cards

- If cash is tight, pay minimums on everything except the card closest to its limit

If you’re carrying credit card debt and can’t pay in full every month, focus on getting current first. None of these credit score strategies replace the basics: don’t spend more than you earn, and pay off high-interest debt before optimizing rewards.

3. Time Your Payments Before the Statement Date

Most people pay their credit card bill before the due date. Smart move. But there’s a timing play that most people miss.

Your credit card issuer reports your balance to the bureaus on your statement closing date, not your payment due date. If you pay down your balance before the statement closes, the reported balance is lower, which means lower utilization on your credit report.

Say your statement closes on the 15th and your payment is due on the 10th of the next month. If you make a big purchase on the 5th and pay it off on the 12th (before statement close), that purchase never shows up as a reported balance.

This is a free move. Same money, same spending, better score.

4. Request a Credit Limit Increase

Alternatively, you can lower your utilization without paying down debt by increasing your ceiling. If your utilization is 30% on a $10,000 limit, and you get bumped to $20,000, your utilization drops to 15% with the same balance.

Fortunately, many issuers let you request an increase through their app or website. Some do a soft pull (no impact on your score), others do a hard pull. Before you request, call or chat and ask which type of inquiry they’ll run.

Chase, Amex, and Capital One are generally known for soft-pull credit limit increases when requested through their apps. Always confirm before requesting, since policies can change.

5. Become an Authorized User on a Responsible Account

If someone you trust (parent, spouse, sibling) has a credit card with a long history and low utilization, getting added as an authorized user can boost your credit score significantly. Their account history, credit limit, and payment record get added to your credit report.

In fact, you don’t even need to use the card. Just being listed as an authorized user gives you the benefit of their account age and credit limit.

A few things to verify first:

- The primary cardholder has a clean payment history on that account

- Their utilization on that card is under 10%

- The issuer reports authorized user accounts to the credit bureaus (most major issuers do)

This strategy is especially powerful for someone early in their credit journey who doesn’t have many accounts yet. If a parent adds you to a card they’ve held for 15 years, your average account age jumps significantly overnight.

Free Credit Card Strategy Tools

Get the ROI Calculator, Points Toolkit, and more. I’ll send them straight to your inbox.

6. Check Your Credit Reports for Errors

A Federal Trade Commission study found that roughly 1 in 5 consumers had an error on at least one of their credit reports (the study is from 2013, but no updated equivalent has been published since). Some of those errors are minor, but some are score-killers: accounts that aren’t yours, late payments that were actually on time, or closed accounts still showing as open with a balance.

Luckily, you get free weekly credit reports from all three bureaus (Equifax, Experian, and TransUnion) through AnnualCreditReport.com. Pull all three. They often have different information.

If you find an error, dispute it directly with the bureau reporting it. The bureau has 30 days to investigate and respond. If the error was dragging down your score, fixing it can produce an immediate bump.

7. Keep Old Credit Cards Open

Closing an old credit card feels like cleaning up, but the math works against you in two ways.

First, you lose that card’s credit limit, which increases your overall utilization. If you have $30,000 in total limits and close a card with a $10,000 limit, your available credit drops to $20,000. Same balances, higher utilization ratio.

On top of that, while closed accounts stay on your report for up to 10 years, they stop aging. Over time, closing old accounts can lower your average account age, which impacts the 15% length-of-history factor.

If the card has no annual fee, keep it open. Put a small recurring charge on it (a streaming subscription works) and set up autopay. If it has an annual fee you can’t justify, call the issuer and ask to product-change it to a no-fee version. That preserves the account age and credit limit. Cards like the Chase Sapphire Preferred can often be downgraded to a no-fee Freedom card while keeping the credit line intact. And if you’re looking for a solid no-fee card to keep active, the Wells Fargo Autograph earns 3X on six categories with zero annual fee.

8. Diversify Your Credit Mix

Credit mix is only 10% of your score, so don’t lose sleep over it. However, if you only have credit cards and no installment loans (auto, mortgage, student, personal), adding one can help.

That said, don’t take out a loan just for your credit score. But if you’re already planning a purchase that involves financing, know that having both revolving credit (cards) and installment credit (loans) in your profile is a positive signal to the scoring model.

For example, credit-builder loans from credit unions are another option. These are small loans ($300-$1,000) specifically designed to build credit history. The money goes into a savings account, and you make payments over 6-24 months. When the loan is paid off, you get the money back plus a stronger credit profile.

9. Space Out Your Credit Applications

Every time you apply for a new credit card or loan, the lender does a hard inquiry on your credit report. Each hard inquiry can drop your score by 2-5 points, and multiple inquiries in a short window signal risk to lenders.

There’s an exception: rate shopping for a mortgage, auto loan, or student loan. FICO treats multiple inquiries of the same type within a 45-day window as a single inquiry in newer scoring models (older models use a 14-day window), so you can shop rates without penalty.

In contrast, for credit cards there’s no such bundling. If you apply for three cards in a month, that’s three separate hard inquiries. Space your credit card applications at least 3-6 months apart, especially if you’re actively building your score.

10. Use Experian Boost and Similar Tools

Experian Boost is a free tool that lets you add utility payments, phone bills, streaming services, and even rent payments to your Experian credit report. If rent is a big part of your monthly spend, cards like the Bilt credit card also report rent payments and earn points on them with no fee. For people with thin credit files, this can add an average of 13 points (per Experian’s own data) by showing consistent payment behavior on accounts that don’t traditionally report to the bureaus.

Similar services include UltraFICO (which factors in banking behavior) and some rent-reporting services. Newer scoring models like FICO 10T and VantageScore 4.0 are also starting to incorporate utility and rent payments natively. These tools work best for people who are just starting to build their credit score and don’t have a long credit card history yet.

11. Be Strategic with Your Credit Usage

If you have cash set aside for a planned purchase, put it on your credit card and pay it off immediately. You earn rewards, build payment history, and show activity on your account.

Just remember, the key word is “immediately.” This strategy only works if the money is already in your bank account before you swipe. If you’re charging purchases you can’t pay off in full, you’re not building credit. You’re building debt.

For example, say you’re paying for a $3,000 home project in cash. Charge it to a card that earns 2% cash back, then pay the statement balance in full. You earn $60 in rewards, add a positive payment to your history, and your score stays clean. That’s not a trick. That’s just good financial operations.

I built a free strategy tracker that helps you run exactly this kind of math. Get it here

How Fast Can You Raise Your Credit Score?

Most people I work with find $300–$800/year in missed rewards from one wrong card or one misassigned category. I map your real spending and build a custom plan in a 30-minute call.

Not financial advice. Results vary by individual spend.

Naturally, the timeline depends on what’s dragging your score down. Here’s a realistic breakdown:

Within 30 days:

- Pay down balances below 10% utilization: potential 20-50 point jump

- Get added as an authorized user: potential 10-30 point increase

- Dispute and resolve a credit report error: varies widely, but can be significant

Within 90 days:

- Request credit limit increases (soft pull) and let lower utilization report

- Sign up for Experian Boost with 3+ months of utility payment history

- Establish consistent on-time payments across all accounts

Within 6-12 months:

- Build a pattern of 100% on-time payments

- Let new accounts age past the “new credit” penalty window

- Diversify credit mix if appropriate

1-2 years:

- Average account age increases, strengthening the length-of-history factor

- Hard inquiries fall off after 2 years

- Consistent behavior compounds into a strong score

Most people overestimate how long it takes to go from a 650 to a 720 and underestimate how long it takes to go from a 720 to an 800. The first jump can happen in 3-6 months with the right moves. The second is a patience game measured in years.

If you want someone to look at YOUR specific card setup and map out a custom optimization plan, I offer 1:1 Spend Audits where I break down your spending categories and find the gaps.

Final Thoughts

Your credit score is a tool. Like any tool, it works better when you understand how it’s built and which parts do the heavy lifting.

The biggest wins come from utilization and payment history. Those two factors alone control 65% of your FICO score. Get those right and you’re ahead of most people. If you want the full playbook of moves before you open your next card, the Credit Card Strategy archive covers every angle. Layer in the timing strategies, authorized user plays, and credit report monitoring, and you’re running a system instead of guessing.

What’s your current credit score range, and which strategy are you trying first? Drop a comment or reach out.

How to Improve Credit Score FAQs

How long does it take to improve your credit score?

It depends on what’s pulling your score down. Lowering credit utilization can boost your score within one billing cycle (about 30 days). Building a strong payment history takes 6-12 months of consistency. Recovering from a late payment or collection takes longer, since negative marks stay on your report for seven years, though their impact decreases over time.

Does checking your own credit score hurt it?

No. In reality, checking your own score is a soft inquiry and has zero impact on your credit. Check it as often as you want. Most major card issuers provide free FICO score access through their apps, and services like Credit Karma provide VantageScore updates weekly.

What is a good credit score to buy a house?

Most conventional mortgage lenders require a minimum score of 620, but you’ll get significantly better interest rates at 740+. FHA loans can go as low as 580 with a 3.5% down payment. The difference between a 680 and a 760 on a $400,000 30-year mortgage could mean over $50,000 in total interest savings over the life of the loan.

Can you improve your credit score by 100 points in 30 days?

Essentially, it’s possible but only in specific situations. If you have very high credit utilization (50%+) and pay it all down at once, the utilization drop alone could add 50-80 points. Combine that with a resolved credit report error, and you might hit 100. For most people, a realistic 30-day improvement is 20-50 points from utilization optimization.

How often is your credit score updated?

Your credit score updates whenever a lender or creditor reports new information to the bureaus, which typically happens once per month per account. Most credit card issuers report your balance on the statement closing date. There’s no single “update day” since different accounts report at different times throughout the month.

Chase Sapphire Preferred

Best mid-tier travel card for beginners. Transfer to Hyatt, United, Southwest.

$95/yr

Wells Fargo Autograph

3x on restaurants, travel, gas, transit, streaming, phone plans. Transfer partners.

$0/yrTerms apply. Some links are affiliate links. I only recommend products I personally use or genuinely believe will help you. Pay your balance in full.

I’m not a financial advisor or CPA. This is personal experience and opinion. Credit card terms and issuer policies can change. Verify current terms with the issuer before making decisions. Terms apply. Pay your balance in full. Applying for credit results in a hard inquiry.

Join the discussion

Prompt

What's your experience with this card or strategy? Share your numbers.

Be the first to share your numbers

Real datapoints from the comments make this thread more useful than another review post.

Leave a comment