Bilt Obsidian + Sapphire Preferred: Best Duo?

Whether you love or hate the new Bilt cards, the 2.0 launch was a mess. The reward structures are confusing, the backlash is loud, and most breakdowns online are treating these cards as standalone options. But here is what nobody is talking about: what happens when you pair the Bilt Obsidian credit card with the Chase Sapphire Preferred?

I’ve been critical of Bilt in the past, and my trust in their issuer Cardless is genuinely in doubt. But you are not me. And when I ran the numbers on this duo, the Obsidian kept hitting in all the right areas. Not because the benefits are flashy, but because the math just works, especially if housing is one of your biggest bills.

In this post, I’m breaking down what each card brings to the table, why they fit together so well, and then putting this duo head-to-head against the three setups everyone recommends: Amex Gold + BBP, Citi Strata Premier + Double Cash, and Capital One Venture X + Savor. That way you’ll know for sure if the “Obsidian Preferred” (my nickname for this combo, you heard it here first) deserves the crown.

Key Takeaways:

- The CSP + Bilt Obsidian duo earns a 2.64% return on total spend (including housing), beating the Amex Gold + BBP at 2.34% and the Capital One duo at 1.87%.

- Excluding housing, the effective return jumps to 6.46% thanks to the Bilt Cash housing lever mechanism.

- Both cards cost $95 each ($190 total), making this the most affordable premium duo on this list.

- The strategy works best for renters or homeowners spending $2,000+/month on housing with consistent non-housing spend to fuel the Bilt Cash engine.

| Bilt Obsidian Black | Chase Sapphire Preferred | |

|---|---|---|

| Annual fee | $95/yr | $95/yr |

| Welcome bonus | $200 Bilt Cash | 75K UR · $5K/3mo |

| Top earn rates | Flexible 4% Bilt Cash · Dining or Groc. 3x · Travel 2x | Chase Travel Portal 5x · Dining 3x · Streaming 3x |

| Top partners | Hyatt · Alaska · Air France-KLM See all → | Hyatt · United · Southwest See all → |

| Card network | Mastercard World Elite | Visa Signature |

| Foreign tx fee | 0% | 0% |

| Best for | Housing-heavy spenders: groceries at effective 4.33X + housing lever | Dining, streaming, travel gaps filled with stronger Visa protections |

| Not for | Non-housing spenders or anyone avoiding Bilt/Cardless complexity | Primary travel card via portal 5X optimization |

| Apply Now → | Apply Now → |

Annual fee

Welcome bonus

Top earn rates

Top partners

Card network

Foreign tx fee

Best for

Not for

BILT OBSIDIAN BLACK

Apply Now →CHASE SAPPHIRE PREFERRED

Apply Now →Terms apply. Some links are affiliate links. Credit card comparisons assume you pay your balance in full every month. Offers shown reflect what was current at publication date.

Bilt Obsidian Credit Card: The Backbone of This Duo

Want to run this math on your spending? Plug in your real numbers and see what each card actually earns you.

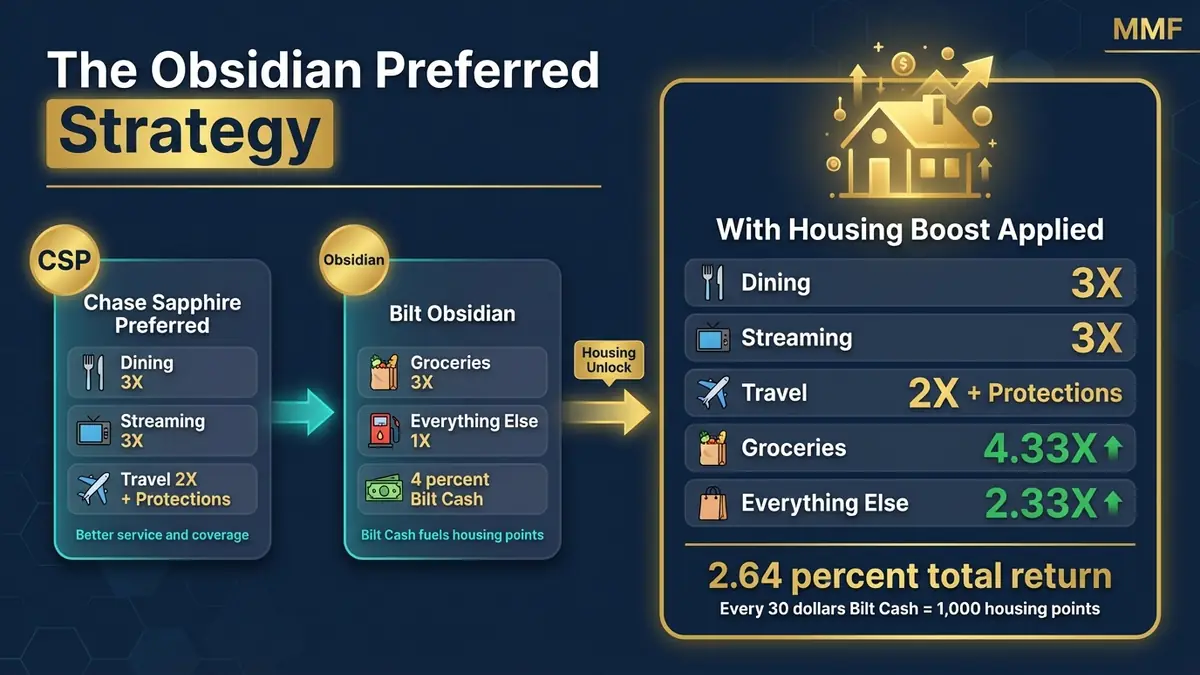

Free Calculator →Every review out there is comparing the Bilt Obsidian against the Sapphire Preferred, as if you have to pick one. That framing misses the point entirely. These two cards aren’t competitors. They’re complements.

The Bilt Obsidian comes with a $95 annual fee (as of April 2026) and a welcome offer of $200 in Bilt Cash. The core pitch is points on housing plus an elevated multiplier in either dining or groceries.

Here’s the earn structure:

- 3X on dining OR groceries (you choose annually, grocery capped at $25,000/year)

- 2X on travel

- 1X on other everyday purchases

- Up to 1.25X on rent + mortgage (earned through Bilt’s tiered system or by redeeming Bilt Cash, not a flat multiplier)

- 4% back in Bilt Cash on everyday spend

Now if you’re confused about the Bilt Cash math, I broke it down in detail in my Bilt Palladium vs Venture X breakdown. But here’s the short version: for every $30 in Bilt Cash earned, you can unlock 1,000 points on your rent or mortgage. When you do this, your effective multiplier jumps +1.33X on up to 75% of your non-housing spend.

That turns the effective multipliers into:

- 4.33X on dining or groceries

- 3.33X on travel

- 2.33X on everything else

On paper, this Bilt Mastercard looks like it would cook. And it does, but only when you pair it correctly.

If you’re building out your credit card strategy and want free tools to run the numbers on any card combination, I’ve got you covered.

Grab the free Rewards & Returns Toolkit

The card also comes with a $100 Bilt Travel Hotel credit per year, split semi-annually, usable on eligible hotel bookings through the Bilt Travel Portal (minimum 2-night stay requirement). Plus Mastercard purchase and travel protections, though as we’ll see, the Sapphire Preferred’s Visa protections are stronger.

Where the Obsidian Thrives in This Setup

Here’s where the Obsidian locks in for this duo:

- 3X multiplier on groceries (choose groceries as your annual category)

- Points on your housing via the +1.33X Bilt Cash boost

- Shared transfer partners with Hyatt, Aeroplan, United, Alaska Atmos, and 1:1 transfers with JAL

The Obsidian is the diamond in the rough of the Bilt 2.0 lineup. As much as I hate to admit it, because Bilt’s entire 2.0 structure is confusing and overcomplicated, this card is an insanely powerful mid-tier option for anyone whose housing payment is their biggest monthly bill.

Chase Sapphire Preferred: The Glue

Most people completely misunderstand what the Sapphire Preferred is actually doing in a multi-card setup. It’s not about earning the most points. It’s about filling every gap the Obsidian leaves open.

The Chase Sapphire Preferred comes with a $95 annual fee and a standard welcome bonus of 75,000 Ultimate Rewards points for $5K in spend (as of April 2026).

Earn Structure

- 5X on travel booked through Chase Travel

- 3X on dining (including takeout and delivery)

- 3X on online groceries (excludes Walmart, Target, wholesale clubs)

- 3X on select streaming

- 2X on all other travel

- 1X everywhere else

- 10% anniversary points bonus (10% of total yearly spend as bonus points)

The CSP is fairly simple: it’s a dining-and-travel engine that quietly boosts your entire year with that 10% anniversary bonus.

Credits and Perks

In addition to solid multipliers, you get a $50 annual hotel credit (statement credit on hotel stays booked via Chase Travel), partner perks like DashPass, and 5X on Lyft rides through 9/30/2027.

Now, I’m not going to lie and say these credits are amazing. Some of them could use a refresh. However, it’s not unreasonable to pull $50+ in value per year from the credits and anniversary bonus as a casual traveler.

The Underrated Part: Travel and Purchase Protection

This is one of the most underrated aspects of the CSP, and it’s why I call it the glue of this setup:

- Trip Delay Reimbursement: up to $500 per ticket for delays of 12+ hours or overnight stay

- Baggage Delay: $100/day up to 5 days (after 6+ hour delay)

- Lost Luggage Reimbursement: up to $3,000 per covered person per trip

- Primary Auto Rental Collision Damage Waiver (state-dependent, secondary in NY)

- Purchase Protection: covers new purchases for 120 days

- Extended Warranty: extends manufacturer warranties up to $10,000 per claim, $50,000 per account

What the CSP Brings to This Duo

Here’s what the CSP brings to this duo:

- 3X multipliers on dining and streaming (categories you’d waste at 1X on the Obsidian)

- Best-in-class purchase and travel protection for a $95 card

- Transfer partner overlap with Bilt on Hyatt, United, and Aeroplan, so both cards feed into the same redemption pools

- 10% anniversary bonus that quietly adds value across your total Chase spend

The Duo Strategy: Which Card for Which Category

Now that you understand each card individually, here’s how they work together. This is where the setup gets interesting.

Use the CSP for:

- Dining: 3X UR (instead of the Obsidian’s 1X or 3X if you chose dining)

- Select streaming: 3X UR

- Travel: 2X UR (even though the Obsidian’s effective rate is higher at 3.33X, I’d rather take Chase’s customer service and travel protections over Bilt and Cardless)

Use the Obsidian for:

- Groceries: 3X Bilt points (choose groceries as your annual 3X category)

- Gas: 1X Bilt points + 4% Bilt Cash

- All other spend: 1X Bilt points + 4% Bilt Cash

- Housing: use your accumulated Bilt Cash to unlock points

The Obsidian handles your two biggest non-dining categories (groceries and housing), while the CSP covers dining, streaming, and travel with better protections. Both cards share transfer partners like Hyatt and United, so your points work toward the same redemptions regardless of which card earned them.

Choose groceries as your annual 3X category on the Obsidian, not dining. The CSP already covers dining at 3X, so doubling up there wastes the Obsidian’s category selection. Groceries at 3X on the Obsidian, boosted to an effective 4.33X with the housing lever, is where the real value lives.

The Spend Analysis: Does the Math Actually Work

For this analysis, I’m using a baseline single-person monthly spend:

- Dining: $225

- Groceries: $400

- Streaming: $70

- Housing: $2,100

- Travel: $130

- Gas: $125

- All other: $500

Total: $3,550/month, or $42,600/year.

I’m breaking this down two ways. First, your overall return on total spend including housing. Second, your return excluding housing, because even though Bilt lets you earn points on housing, you’re really unlocking those points based on your spend in other categories, not paying your rent on a credit card.

I went deeper on this with the full math in the video, worth watching if you want to see it live.

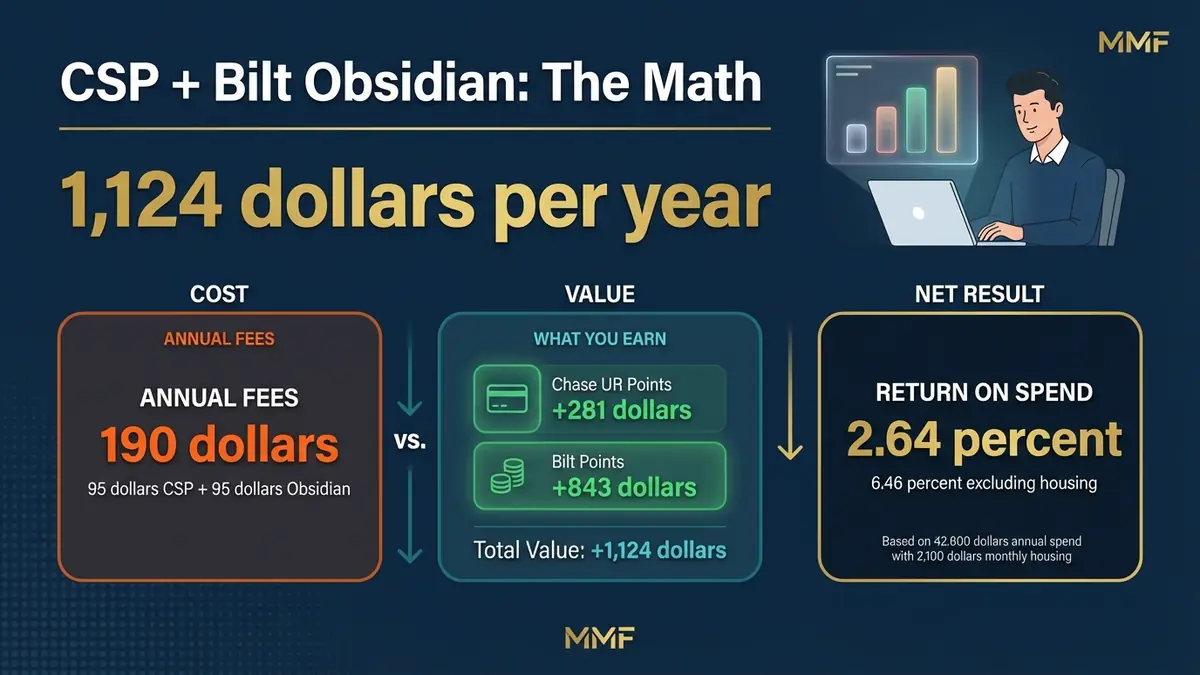

CSP Earnings

- Dining: $2,700/year at 3X = 8,100 UR

- Streaming: $840/year at 3X = 2,520 UR

- Travel: $1,560/year at 2X = 3,120 UR

CSP total: 13,740 Ultimate Rewards. At 2.05 cents per point, that’s $281.67 in value.

Obsidian Earnings

- Groceries: $4,800/year at 3X = 14,400 Bilt points

- Gas: $1,500/year at 1X = 1,500 Bilt points

- All other: $6,000/year at 1X = 6,000 Bilt points

Obsidian subtotal: 21,900 Bilt points before housing.

The Housing Lever

This is where the math flips. Your non-housing spend on the Obsidian is $12,300/year. At 4% Bilt Cash, that generates $492 in Bilt Cash.

If your rent or mortgage processing fee is 3%, that $492 covers the fee on $16,400 in housing payments. And that unlocks 16,400 Bilt points at 1X, without you paying a dime out of pocket for fees.

Total Bilt points: 21,900 + 16,400 = 38,300 Bilt points. At 2.2 cents per point, that’s $842.60 in value.

Combined duo value: $281.67 (CSP) + $842.60 (Obsidian) = $1,124.27 per year. That’s a 2.64% return on total spend including housing, and an effective 6.46% on non-housing spend alone.

That $1,124 is based on a sample budget, yours will be different. Most people I work with are leaving $300-$800/year on the table from one wrong card, one misassigned category, or one annual fee that doesn’t pencil out. I run 1:1 Spend Audits: I map your real spend, check your issuer rules, and hand you a written optimization plan you can execute the same week. Book a Spend Audit ($97)

For this analysis, I’m assuming Bilt is the only way to earn points on housing. You could potentially pay rent on a credit card directly, but the processing fee wouldn’t be worth it for everyday spend. For mortgages, that’s not even possible. So if you don’t use Bilt, the return on your housing category is effectively 0%.

If you want to run these numbers for your own spend, I built a free Credit Card ROI Calculator that breaks down your return by category for any card. Get it here

Head-to-Head vs the Big Three Duos

Most people I work with find $300–$800/year in missed rewards from one wrong card or one misassigned category. I map your real spending and build a custom plan in a 30-minute call.

Not financial advice. Results vary by individual spend.

The Obsidian Preferred sort of cooks. But does that one housing lever mechanism actually move the needle enough to beat the three most popular two-card setups? Let’s find out.

Amex Gold + Blue Business Plus

Housing earns zero on this setup.

- Amex Gold: dining at 4X = 10,800 MR, groceries at 4X = 19,200 MR

- BBP covers the rest at 2X

Total: 49,800 MR points, worth $996 at 2 cents per point.

That’s a 2.34% return on total spend (housing included), or 5.72% on non-housing spend.

If your travel is mostly flights and you capture 3X instead of 2X on some categories, the total return bumps to about 2.41%. The ranking doesn’t change.

Citi Strata Premier + Double Cash

No housing points with this setup either.

Total: 45,360 ThankYou points. At 1.9 cents per point, that’s $861.84.

That works out to a 2.02% total return and 4.95% on non-housing spend.

Capital One Venture X + Savor

Same story: your rent or mortgage earns nothing here.

If you don’t portal-optimize travel, you get 43,140 miles, worth $798.09 at 1.85 cents per mile.

That’s a 1.87% total return and 4.59% on non-housing spend.

If you book travel through the Capital One portal at 5X for flights, the total jumps to about 2.08%. Still not enough.

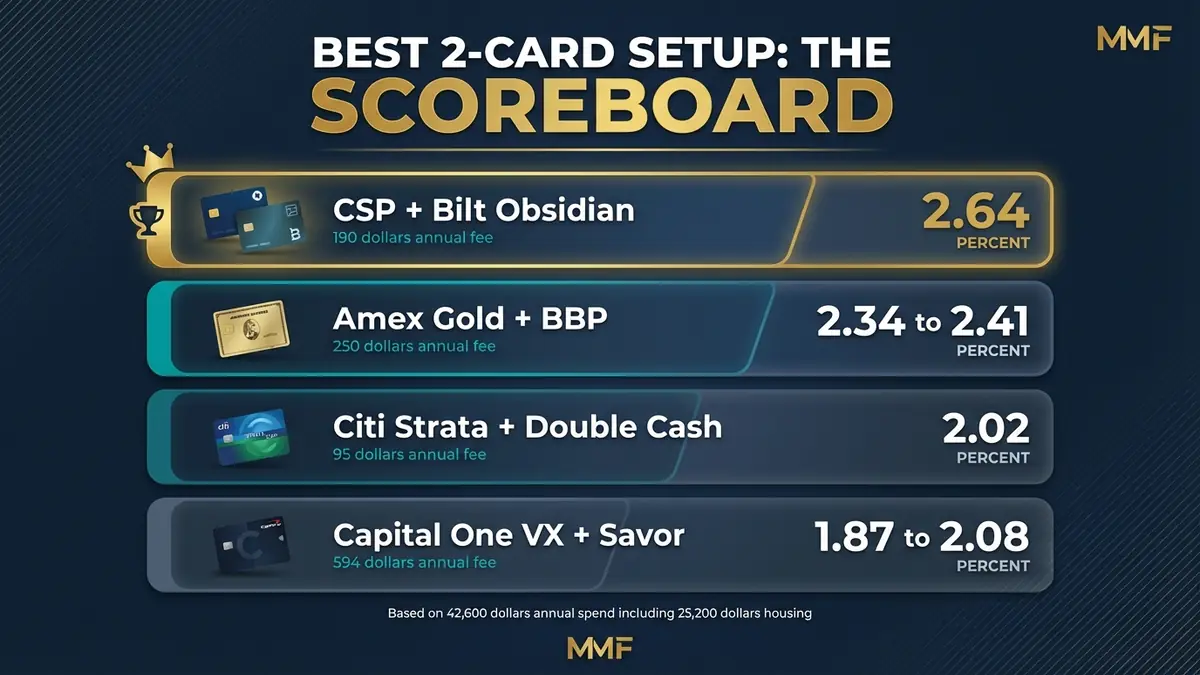

The Final Scoreboard

| Duo | Total Return | Non-Housing Return | Combined Annual Fee |

|---|---|---|---|

| CSP + Bilt Obsidian | 2.64% | 6.46% | $190 |

| Amex Gold + BBP | 2.34-2.41% | 5.72% | $325 |

| Citi Strata + Double Cash | 2.02% | 4.95% | $95 |

| Capital One VX + Savor | 1.87-2.08% | 4.59% | $395 |

The CSP + Obsidian duo wins on raw earning power at the lowest combined annual fee on this list. The Capital One duo costs $395/year and comes in last on returns. Now, this doesn’t account for the Venture X’s lounge access or the Amex Gold’s dining credits. Those have value too. But purely on the math of earning potential per dollar spent, the Obsidian Preferred combo is the best credit card setup for under $200 in 2026.

Best For / Not For

Who Should Run the Obsidian Preferred Duo

Best for:

- Renters or homeowners with housing payments of $2,000+/month who want to earn points on that spend

- Card optimizers who don’t mind managing two cards and the Bilt Cash system

- Travelers who value transfer partner access to Hyatt, United, Aeroplan, and JAL across both ecosystems

- Anyone looking for the highest earning two-card setup for under $200/year in fees

Not for:

- Anyone carrying credit card debt. Pay that off first, then come back to this strategy

- People who want simplicity and don’t want to track Bilt Cash unlocks and category selections

- Frequent flyers who rely on lounge access (neither card offers lounges)

- Cardholders who distrust Bilt or Cardless and would rather stick with established issuers like Chase, Amex, or Capital One exclusively

This strategy requires consistent non-housing spend to fuel the Bilt Cash engine. If your monthly non-housing spending is under $1,000, you won’t generate enough Bilt Cash to unlock meaningful housing points, and the effective earn rate advantage over simpler setups shrinks significantly.

If you’re just starting to build credit and aren’t ready for a multi-card strategy yet, check out this beginner’s guide to credit cards for building credit first.

The Bilt Obsidian paired with the Chase Sapphire Preferred is the highest-earning two-card setup I’ve found in 2026 for anyone whose housing payment is their biggest monthly expense. At $190/year in combined fees, you’re getting 2.64% total return on every dollar you spend, including rent or mortgage. The housing lever is what separates this from every other duo on the market. Is it more complex than an Amex Gold + BBP setup? Yes. Does the math justify that complexity? The numbers don’t lie.

CSP + Bilt Obsidian Duo Rating: 4.4/5. Top-tier earning power at a budget annual fee, held back only by Bilt’s complexity and Cardless’s reputation.

Final Thoughts

This isn’t as straightforward as it seems. There are cards on this list with better travel protections, better lounge access, or easier-to-use credits. And the issue of Cardless’s customer service is real.

But that’s not the point of this analysis. The point is: for a two-card setup under $200 in annual fees, with top-tier multipliers and overlapping transfer partners, the Obsidian Preferred needs to be on your radar. For more head-to-heads and duos, the full Credit Card Reviews library has every breakdown.

If you want the full spreadsheet system I use to track stacks like this: Rewards & Returns Toolkit

Let me know your thoughts. Is the Obsidian Preferred the best credit card duo of 2026, or do you think another setup wins even though the earning might be less?

Bilt Obsidian Credit Card FAQs

Is the Bilt Obsidian credit card worth the $95 annual fee?

For most people who pay rent or a mortgage, yes. The $100 Bilt Travel Hotel credit offsets most of the fee, and the 4% Bilt Cash on everyday spend creates meaningful housing points when redeemed properly. The real value comes from pairing it with a card like the CSP that covers its weak categories (dining and travel protections). If housing isn’t a major expense for you, a simpler card like the Wells Fargo Autograph might be a better fit.

How does the Bilt Cash housing lever actually work?

Every dollar you spend on non-housing purchases earns 4% back in Bilt Cash. For every $30 in Bilt Cash you accumulate, you can unlock 1,000 Bilt points on your rent or mortgage payment. This effectively adds +1.33X to your earn rate on up to 75% of your non-housing spend. So a 3X grocery category becomes an effective 4.33X, and 1X everyday spend becomes an effective 2.33X.

Can you use both Bilt and Chase transfer partners with this duo?

Yes, and that’s one of the biggest advantages. Both Bilt and Chase Ultimate Rewards transfer to Hyatt, United, and Aeroplan. This means whether your points are in your Bilt account or your Chase account, you can funnel them toward the same hotel or airline redemptions. JAL is a Bilt exclusive, and Southwest is a Chase exclusive, so you also get broader coverage.

Is the Bilt Obsidian better than the Amex Gold for groceries?

On paper, the Amex Gold earns 4X on groceries versus the Obsidian’s 3X. However, when you factor in the +1.33X housing boost from Bilt Cash, the Obsidian’s effective grocery rate becomes 4.33X. If housing is a major expense, the Obsidian pulls ahead in total value even with a lower base multiplier.

What’s the biggest risk of this credit card setup?

Bilt’s issuer, Cardless, has a weaker reputation for customer service compared to Chase, Amex, or Capital One. If something goes wrong with a charge, dispute, or account issue on the Obsidian side, you’re dealing with a less established operation. That’s why this strategy puts travel purchases on the CSP, where Chase’s customer service and Visa Signature protections provide a stronger safety net.

Bilt Obsidian Black

3x dining or grocery (select annually), 2x travel. $100/yr Bilt Hotel credit. 4% Bilt Cash flexible. Up to 1.25x housing.

$95/yr

Bilt Palladium

2x everyday, 4% Bilt Cash flexible. $400/yr hotel credit, $200 Bilt Cash, Priority Pass. Up to 1.25x housing.

$495/yr

Bilt Blue

Earns points on rent with no annual fee. 1x everyday or 4% Bilt Cash (flexible). Up to 1.25x on housing.

$0/yr

Chase Sapphire Preferred

Best mid-tier travel card for beginners. Transfer to Hyatt, United, Southwest.

$95/yr

Wells Fargo Autograph

3x on restaurants, travel, gas, transit, streaming, phone plans. Transfer partners.

$0/yr

American Express Gold Card

4x dining and US supermarkets. $10/mo Uber Cash, $10/mo dining credit, $7/mo Dunkin', $100 Resy credit/yr.

$325/yr

Citi Strata Premier

3x on restaurants, supermarkets, gas/EV, air travel, hotels. 10x via Citi Travel portal. Transfer partners.

$95/yrTerms apply. Some links are affiliate links. I only recommend products I personally use or genuinely believe will help you. Pay your balance in full.

Some links in this article are affiliate links. I only recommend products I personally use or genuinely believe will help you. Terms apply. Pay your balance in full. Applying for a credit card results in a hard inquiry. I’m not a financial advisor or CPA. This is personal experience and opinion.

Join the discussion

Prompt

What's your experience with this card or strategy? Share your numbers.

Be the first to share your numbers

Real datapoints from the comments make this thread more useful than another review post.

Leave a comment