Is the Apple Card Worth It? (The Math Says No for Most)

The titanium card arrives and it feels different from everything else in your wallet. No card number on the front. Clean laser-etching. It gets noticed at restaurants.

That aesthetic is exactly the problem.

For most people who carry the Apple Card as their primary card, the design is effectively subsidized by a worse reward rate than what a dozen free alternatives already offer. This is not about fees. The Apple Card has no annual fee, no late fees, and no foreign transaction fees. That opportunity cost is quieter than that, and it shows up every year when you run the numbers.

I am breaking down the actual reward structure, where the math breaks down, what you are giving up, the Chase acquisition news (and why it matters now), and the two no-annual-fee setups that beat it for 99% of spending patterns.

Key Takeaways:

- Earn rates: 3% at Apple and select partners with Apple Pay, 2% on other Apple Pay purchases, 1% with the physical card

- Blended return on a realistic $2,000/month spend: roughly 1.8%, or $432/year

- A flat 2% card earns $480 on that same $24,000 with zero ecosystem requirements

- Welcome bonus: $75 is the weakest offer in the no-fee category, comparable cards offer $200 or more

- JPMorgan Chase officially confirmed in January 2026 that it is taking over the card from Goldman Sachs, and that changes one specific scenario worth knowing about

| Apple Card | Citi Double Cash | Fidelity Rewards Visa Signature | |

|---|---|---|---|

| Annual fee | $0/yr | $0/yr | $0/yr |

| Top earn rates | Apple/Partners (AP) 3% · Apple Pay 2% · Physical Card 1% | Everything 2% | Everything 2% |

| Top partners | None | American Airlines · Turkish Airlines · Virgin Atlantic See all → | None |

| Card network | Mastercard | Mastercard | Visa Signature |

| Foreign tx fee | 0% | 3% | 0% |

| Best for | Heavy Apple Pay users with multiple Apple subscriptions who want $0 fees and zero maintenance | Flat 2% on everything with a future upgrade path to ThankYou Points and 18 transfer partners | Simplest 2% flat with auto-deposit into Fidelity account and a Global Entry credit every 4 years |

| Not for | Physical card users who regularly slip to 1%, and anyone building a multi-card optimized setup | Anyone who wants transfer partner access without adding a second card | Anyone who prefers cash back outside a Fidelity account |

| Apply Now → | Apply Now → | Apply Now → |

Annual fee

Top earn rates

Top partners

Card network

Foreign tx fee

Best for

Not for

Terms apply. Some links are affiliate links. Credit card comparisons assume you pay your balance in full every month. Offers shown reflect what was current at publication date.

How the Apple Card Actually Pays You

Want to run this math on your spending? Plug in your real numbers and see what each card actually earns you.

Free Calculator →The Apple Card earns Daily Cash back in three tiers: 3% at Apple directly and a short list of select partners including Nike, Uber, and Exxon/Mobil when you pay via Apple Pay; 2% on all other Apple Pay purchases; and 1% when you swipe the physical card or shop at merchants that do not accept Apple Pay.

No annual fee. No foreign transaction fee. No late fees. Overall, the fee structure is genuinely clean.

On the marketing side, Apple executed this brilliantly — building the most attractive physical card on the market, then making the physical card the worst way to earn. Apple built the most attractive physical card on the market and then made using that physical card the worst possible way to earn rewards. If you want the 2% rate, you need to be paying with your phone. Forget your phone, or shop anywhere that does not take contactless payments, and you drop to 1%.

Still, that 1% fallback is not a minor quirk. In fact, it is the structural flaw that makes this card underperform for most users.

If you want free tools to run the numbers on your own card setup, I built a toolkit for exactly this.

Grab the free Rewards & Returns Toolkit

The Math Behind the Opportunity Cost

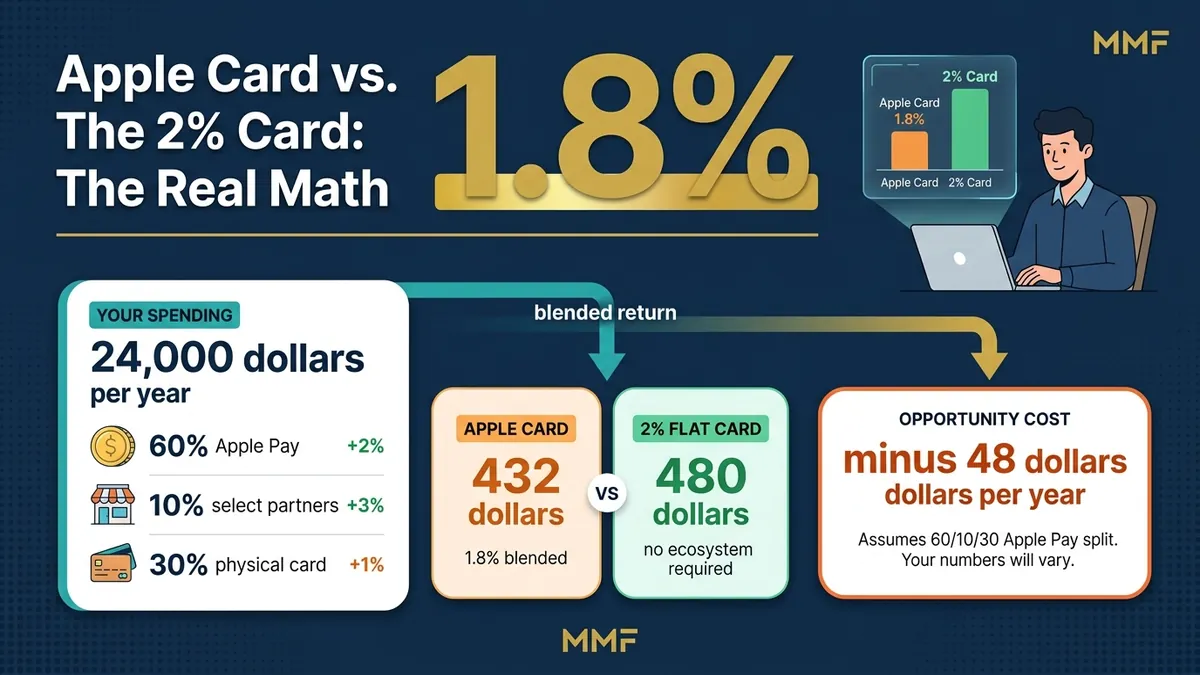

To understand the gap, start with a realistic spend scenario: $2,000 per month, or $24,000 per year. And let’s be generous to the Apple Card on the split: 60% flows through Apple Pay at 2%, 10% hits the 3% partner categories, and the remaining 30% ends up on the physical card or at merchants without Apple Pay support.

Running the Numbers

The breakdown:

- 60% of $24,000 = $14,400 at 2% = $288

- 10% of $24,000 = $2,400 at 3% = $72

- 30% of $24,000 = $7,200 at 1% = $72

- Total: $432/year, a blended rate of 1.8%

By comparison, a flat 2% card on that same $24,000 returns $480. No Apple Pay required, and no ecosystem to manage.

Admittedly, that $48 gap in year one is not catastrophic. But $48 compounded over five years is $240, and that is assuming the 60/10/30 split holds. Shop online frequently, travel internationally, or forget your phone once a week and that 30% at 1% creeps higher fast.

In practice, the real loss shows up when you pair cards. A 3% category card on dining and groceries alongside a 2% catch-all is a combination the Apple Card cannot replicate. The Apple Card forces a binary choice: use Apple Pay and get 2%, or pull out your dedicated category card and lose the catch-all entirely. You cannot run both strategies on the same transaction.

Specifically, that two-card pairing is where Apple Card users routinely leave $200 to $400 extra per year on the table compared to a basic optimized setup.

What the Apple Card Leaves Out

The reward structure is one issue, but the feature list adds to it.

For starters, the Apple Card does not offer a standard 0% intro APR on purchases. If you are planning a major purchase and want to pay it off interest-free over 12 to 15 months, this card gives you nothing. Apple Card Monthly Installments exists but only applies to Apple hardware purchases at checkout, not general spending. Balance transfers aren’t supported either.

Beyond the APR gap, the sign-up bonus is $75 in Daily Cash after spending $75 in your first 30 days. That is a welcome bonus in name only. No-annual-fee cards in the same space regularly offer $200 or more for $500 to $1,000 in spend over three months. That gap is real year-one money you are leaving on the table.

Furthermore, the Apple Card does not include purchase protection or extended warranty coverage on eligible purchases. For a product positioned as premium, that is a notable omission.

The Chase Takeover: What It Actually Means

Most people I work with find $300–$800/year in missed rewards from one wrong card or one misassigned category. I map your real spending and build a custom plan in a 30-minute call.

Not financial advice. Results vary by individual spend.

When I put together the video on this card, the Chase acquisition was still being reported as a rumor. It is confirmed now.

On January 7, 2026, Apple and JPMorgan Chase officially announced that Chase will take over the Apple Card portfolio from Goldman Sachs. The deal covers more than $20 billion in card loans and will take approximately 24 months to fully close. Goldman had been winding down its consumer business since 2022. After American Express, Synchrony, and Barclays all exited negotiations, Chase was the last bank standing.

What Changes (and What Doesn’t)

For now, existing Apple Card holders see no changes. Terms, rates, and rewards stay in place through the transition.

The long-run question is what Chase does with the product. Chase runs the Ultimate Rewards ecosystem, one of the most valuable points currencies in travel. A future product change that connects Apple Card spending to UR points would make this card a completely different conversation. No such announcement has been made, and Chase has said nothing about it publicly.

But it is the one scenario that would turn the Apple Card from a pass into a legitimate option for points chasers. Overall, it is worth watching. Still, it is not worth applying for on speculation.

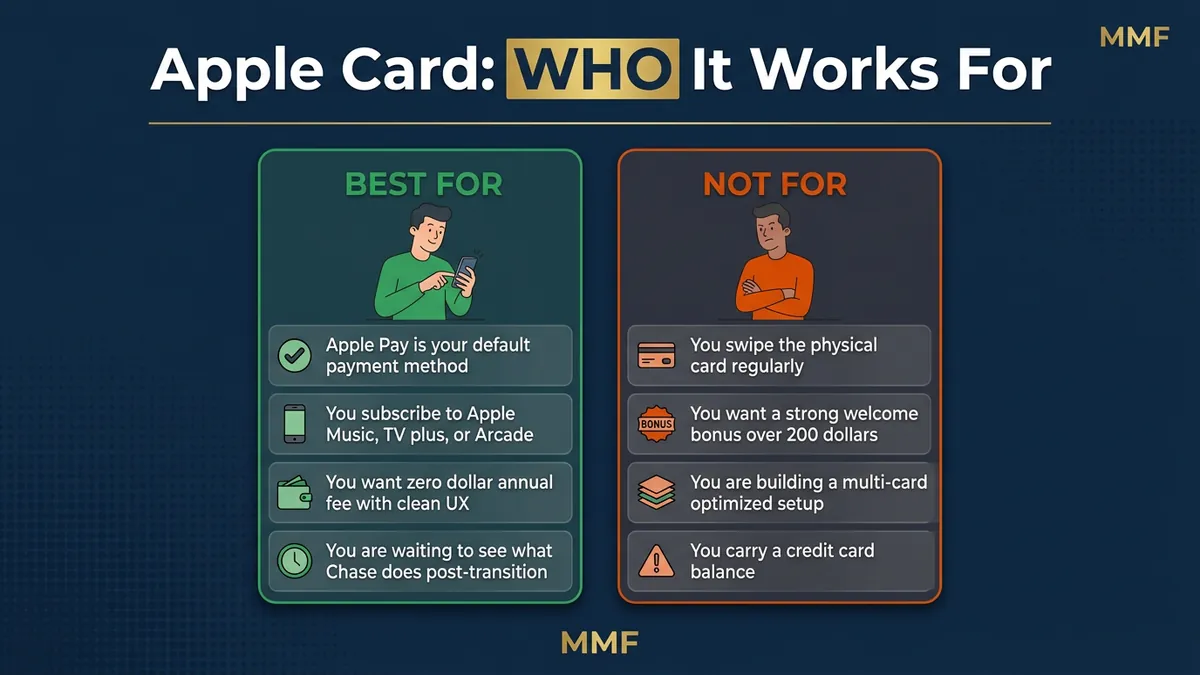

Apple Card: Best For / Not For

Best for:

- iPhone users making 80%+ of purchases via Apple Pay with active Apple subscriptions (Music, TV+, Arcade)

- Anyone who wants a $0 annual fee card with genuinely clean UX and zero fees of any kind

- Current Apple Card holders waiting to see what Chase does with the product post-transition

Not for:

- Anyone who uses a physical card regularly or shops at merchants that do not take Apple Pay

- Users looking for a meaningful sign-up bonus on their first card

- Anyone building a multi-card setup: better catch-all alternatives exist

- Anyone carrying a credit card balance: no 0% intro APR option available

The math above uses a realistic but specific 60/10/30 Apple Pay split. Your actual blended return depends on how often you use Apple Pay versus the physical card. Most people I work with are leaving $200 to $400 per year on the table from one wrong card or misassigned category. The 30-minute Spend Audit maps your real spending and hands you a written optimization plan.

What to Get Instead

Two no-annual-fee setups outperform the Apple Card for most spend patterns.

Fidelity Rewards Visa

The Fidelity Rewards Visa earns a flat 2% back on every purchase, no categories and no Apple Pay requirement. Redemption goes directly into a Fidelity account, which takes about ten minutes to open. The card also includes a $100 credit toward TSA PreCheck or Global Entry every four years. It is a benefit the Apple Card does not offer.

If you want the simplest 2% setup and cash rewards deposited automatically, this is the cleanest option available.

Citi Double Cash

The Citi Double Cash also earns 2%, 1% when you buy and 1% when you pay. What separates it from the Fidelity card is the upgrade path. The Double Cash earns ThankYou Points behind the scenes, and if you ever add a Citi Strata Premier to your wallet, those points become transferable to 18 airline and hotel partners at full value.

You are not locked into cash back forever. In other words, scaling into a points-earning travel setup is possible without switching cards or restarting from zero. The Apple Card has no equivalent path regardless of who the issuer is.

Capital One Savor

If most of your spending falls in dining, groceries, entertainment, or streaming services, the Savor earns 3% across all of those categories with no annual fee. Pair it with a flat 2% catch-all for everything else and your blended rate on a typical spend profile pushes above 2.5%, well ahead of what the Apple Card delivers.

Specifically, the Savor earns 1% outside those categories, so it works as a category card, not a standalone. But a two-card setup is exactly how you outperform a card trying to do everything at 1.8%.

If housing is one of your biggest monthly bills, check out my post on the Bilt Blue Credit Card Review. It’s one of the best no annual fee catch-all cards with an effective 2.33x if used correctly.

Apple Card Review FAQs

Is the Apple Card worth it in 2026?

For most users, no. The Apple Card’s blended return on typical spending lands around 1.8%, which trails simple 2% flat-rate cards with no ecosystem requirements. That said, there is one exception: someone who makes 80% or more of purchases through Apple Pay and carries active Apple subscriptions.

What is the Apple Card welcome bonus?

A promotional $75 Daily Cash offer is currently available for new applicants who spend $75 in the first 30 days. That is far below the $200 or more available on comparable no-annual-fee cards in the same credit tier.

What happens to the Apple Card now that Chase is taking over from Goldman Sachs?

JPMorgan Chase confirmed the acquisition in January 2026. The transition takes approximately 24 months. Card terms, rates, and rewards stay unchanged during that period. A potential future connection to Chase Ultimate Rewards has not been announced and is speculative.

Can you use the Apple Card without Apple Pay?

Yes. The physical titanium card works anywhere Mastercard is accepted. But you earn only 1% cash back with the physical card versus 2% or 3% via Apple Pay. Using the physical card as your primary method makes this a 1% cash back card, below the current market average for no-annual-fee rewards cards.

What credit score do you need for the Apple Card?

The Apple Card is available to applicants with good to excellent credit, typically 700 or higher. Approval is not guaranteed and depends on your full credit profile.

The Apple Card is a well-designed card that performs exactly as advertised inside the Apple ecosystem. However, performing well inside the ecosystem and being the best card for your wallet are not the same thing. “works great inside the Apple ecosystem” and “best card for your wallet” are not the same thing for most users. If you already maximize Apple Pay on every purchase and pay for multiple Apple services, the card performs adequately. For everyone else, a flat 2% card earns more money on the same spend without changing any spending behavior.

Still, the Chase takeover is the first genuinely interesting development in the Apple Card’s history. If a future product change connects Apple Card spend to Ultimate Rewards, the calculus shifts significantly. Until that announcement is official, it is a card to watch, not one to chase.

Drop your Apple Card take in the comments: is it earning its spot in your wallet or is it just the best-looking card in the drawer?

Apple Card

3% Daily Cash at Apple and select partners (Nike, Walgreens, Uber, Exxon) with Apple Pay. 2% all other Apple Pay purchases. 1% physical card. No annual fee, no late fees, no foreign TX fees. Transitioning from Goldman Sachs to JPMorgan Chase (confirmed Jan 2026, ~24-month close).

$0/yr

Fidelity Rewards Visa Signature

Flat 2% cash back on everything, deposited directly into a Fidelity account. $100 Global Entry or TSA PreCheck credit every 4 years. Auto rental CDW up to $75K. No annual fee, no foreign TX fees, no reward caps or expiration.

$0/yr

Citi Double Cash

Flat 2% on everything (1% when you buy + 1% when you pay).

$0/yr

Capital One Savor Rewards

3% dining, entertainment, grocery, streaming. 8% via C1 Entertainment. No annual fee.

$0/yr

Citi Strata Premier

3x on restaurants, supermarkets, gas/EV, air travel, hotels. 10x via Citi Travel portal. Transfer partners.

$95/yr

Citi Custom Cash

5% on your top eligible spend category each billing cycle, up to $500.

$0/yrTerms apply. Some links are affiliate links. I only recommend products I personally use or genuinely believe will help you. Pay your balance in full.

Some links in this post are affiliate links. I only recommend products I personally use or genuinely believe will help you. Card terms apply. Pay your balance in full each month. Applying for a new card results in a hard inquiry on your credit. I am not a financial advisor or CPA. This is personal experience and opinion.

Join the discussion

Prompt

What's your experience with this card or strategy? Share your numbers.

Be the first to share your numbers

Real datapoints from the comments make this thread more useful than another review post.

Leave a comment