Bilt Credit Card Review: Best No-Fee Catch-All?

People either love the Bilt credit card or they hate it. The 2.0 launch was messy, the reward structure is confusing, and most reviews either overhype it or dismiss it entirely.

But here is what the math actually shows: for a specific type of person, the Bilt Blue Card can function as the best no annual fee catch-all card on the market. Not because of some magic multiplier, but because of a Bilt Cash mechanism that most people either misunderstand or ignore completely.

In this post, I’m breaking down the real numbers behind the Bilt Blue Card’s effective 2.33X earn rate, the exact conditions where that math holds up, and a head-to-head comparison against the Citi Double Cash and Chase Freedom Unlimited. By the end, you will know whether this card is worth it for your wallet, or if you should stick with the OGs.

Key Takeaways:

- The Bilt Blue Card can deliver an effective 2.33X points rate on non-housing spend when you use Bilt Cash to unlock housing points

- The strategy works best when your non-housing spend is at or under 75% of your annual housing payment

- If you don’t route housing through Bilt or don’t want to manage the unlock system, the Citi Double Cash at 2% is the cleaner play

- Bilt points transfer 1:1 to partners like Hyatt and Alaska Airlines, giving them premium value

Bilt Credit Card: The 2.33X Math Explained

Want to run this math on your spending? Plug in your real numbers and see what each card actually earns you.

Free Calculator →When you hear “catch-all card,” you probably think 1.5X or 2X flat on everything. Maybe 3X in a couple of bonus categories. But what if a $0 annual fee card could give you an effective 2.33X on your everyday spend?

That is not a typo. And before you think it sounds overhyped, let me walk through the actual math, because this one is grounded in real spend and real unlock mechanics.

The Setup

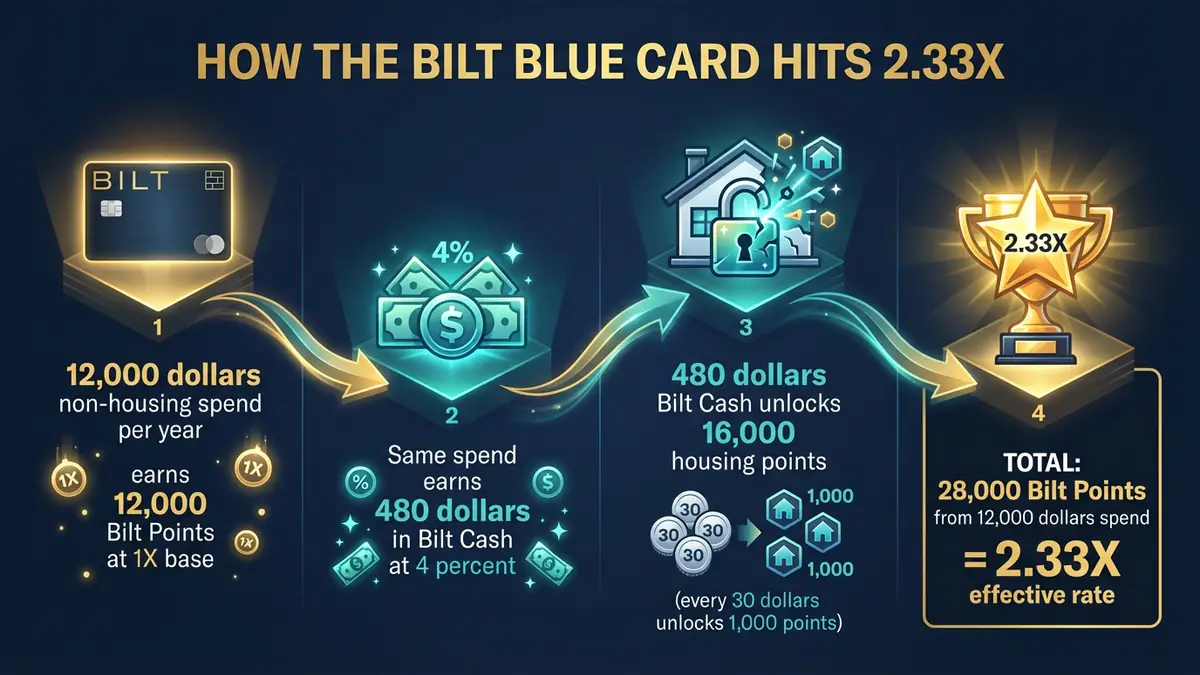

Imagine you pay $2,000 in rent per month, which is $24,000 per year. Then add $1,000 in other monthly spending, another $12,000 annually.

With the Bilt Blue Card, you earn 1X base points on all purchases. You also earn 4% back in Bilt Cash on everyday spend. This assumes you select the “Flexible Bilt Cash” option in the Bilt app, because that is what activates the 4% Bilt Cash earning.

What Is Bilt Cash?

Bilt Cash is Bilt’s own currency inside the Bilt ecosystem. Think of it like credits you can redeem for things like dining perks, partner credits, or (and this is the key part) unlocking points on your housing payment.

Here is how the unlock works: every $30 of Bilt Cash can unlock 1,000 Bilt points on your rent or mortgage.

Running the Numbers

On $12,000 per year of non-housing spend, you earn:

- 12,000 Bilt points (at 1X base)

- $480 in Bilt Cash (at 4%)

That $480 in Bilt Cash unlocks 16,000 additional Bilt points against your housing payment ($480 / $30 x 1,000 = 16,000).

Total points earned: 12,000 + 16,000 = 28,000 Bilt points.

All from $12,000 in non-housing spend.

28,000 points divided by $12,000 in spend = an effective 2.33X catch-all rate on non-housing purchases. That rate holds as long as your non-housing spend stays at or under 75% of your annual housing payment.

If you are building out your credit card strategy and want free tools to run the numbers on any card, I built a toolkit for exactly this.

Grab the free Rewards & Returns Guide

The 75% Rule: When Bilt Blue Works and When It Doesn’t

This is the part where most people mess it up. The 2.33X rate is real, but it only holds under specific conditions. Miss any of them and you are leaving value on the table.

Three Non-Negotiable Conditions

Condition 1: You need a housing payment through Bilt.

If you don’t pay rent or a mortgage through Bilt’s portal, there is nothing to unlock. The entire strategy disappears. This card is built around housing as the unlock bucket.

Condition 2: You must use Bilt Cash to unlock housing points.

Earning Bilt Cash is not enough. You have to actively redeem it to unlock points on your housing. If you choose to use Bilt Cash for dining perks or other redemptions instead, the 2.33X math falls apart.

Condition 3: The 75% ratio matters.

Here is the simple version. If your housing payment is $2,000 per month ($24,000 per year), your non-housing spend needs to stay at or under $18,000 per year to keep the math clean. At that level, all of your earned Bilt Cash converts into housing points without any left over.

The sweet spot formula: multiply your annual housing payment by 0.75. If your total non-housing spend is at or under that number, you are in the zone for the full 2.33X effective rate. Above that, your extra Bilt Cash needs to be redeemed in other ways, and your effective multiplier shifts depending on how you use it.

What Happens Above 75%?

Once your non-housing spend exceeds roughly 75% of your annual housing payment, you will fully unlock 1X on housing, and then you are left with surplus Bilt Cash. That Bilt Cash still has value, but it is not converting into points on housing anymore. At that point, your effective multiplier may be less or greater than 2.33X depending on how you redeem your excess Bilt Cash.

If you are in that situation, there are likely better no-fee catch-all options for you. Which brings us to the competition.

Bilt Blue Card Overview

Before comparing, here is a quick summary of what the Bilt Blue Card actually offers as of April 2026:

- Annual fee: $0

- Base earn rate: 1X Bilt Points on everyday spend

- Earning options (choose one): Flexible Bilt Cash (4% back in Bilt Cash on everyday spend) or Housing-only (up to 1.25X points on rent and mortgage)

- Cell phone protection: Included

- Foreign transaction fees: None

- Welcome offer: $100 in Bilt Cash (as of April 2026)

Why Bilt Points Matter

The real power of Bilt points value is in the transfer partners. Bilt transfers 1:1 to programs like Hyatt, Alaska Airlines, Aeroplan, and Japan Airlines. That is premium transfer partner access on a $0 annual fee card. If you have read my breakdown on the Bilt Obsidian + CSP duo, you know how powerful these partners can be when you combine them with Chase Ultimate Rewards.

For a deeper look at how the Bilt Cash housing lever works at the premium tier, the Bilt Palladium vs Venture X breakdown covers the mechanics in detail.

I went deeper on the full comparison with real numbers in the video, worth watching if you want to see the math play out live.

Bilt Credit Card vs Citi Double Cash vs Chase Freedom Unlimited

Most people I work with find $300–$800/year in missed rewards from one wrong card or one misassigned category. I map your real spending and build a custom plan in a 30-minute call.

Not financial advice. Results vary by individual spend.

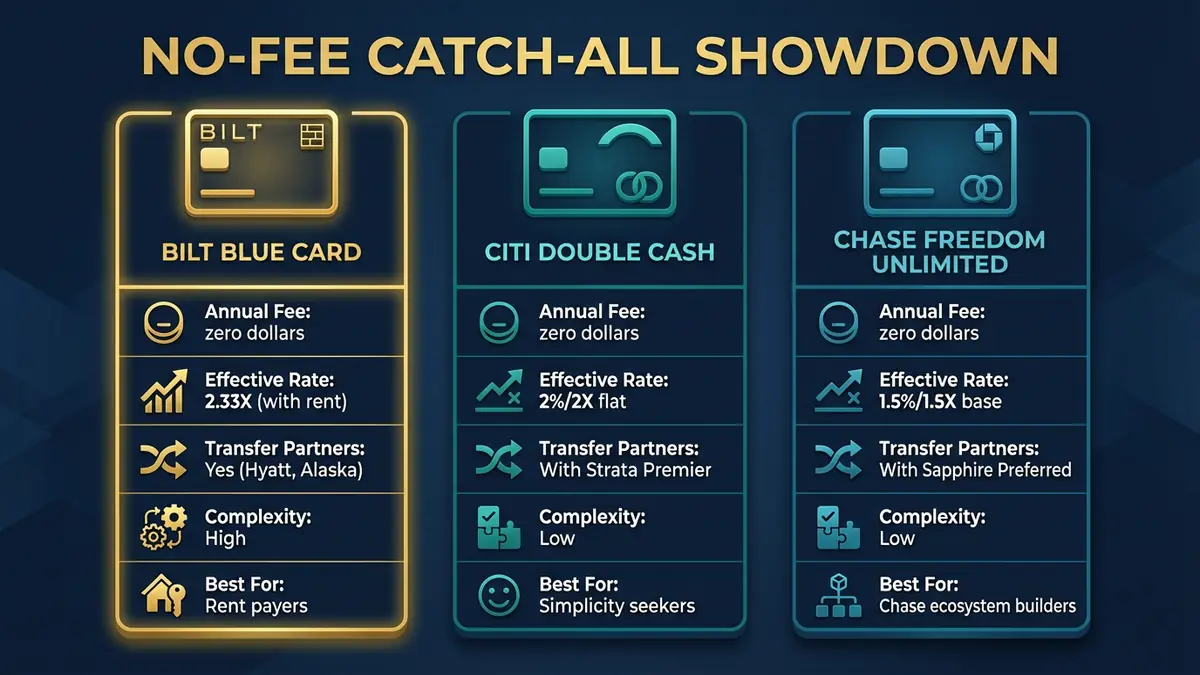

Now the real question: if you are not in the Bilt sweet spot, or you do not want to manage portals and unlock mechanics, what is the best no annual fee catch-all card?

Citi Double Cash: The Simplicity King

No portals. No unlock mechanics. No “you have to redeem it this way or it does not count.”

The Citi Double Cash earns a flat 2% back on everything: 1% when you make a purchase, 1% when you pay it off. That is it. Clean and straightforward.

You can also convert that cash back into ThankYou Points if you pair it with a transferable card like the Citi Strata Premier, which opens up transfer partner access.

If your goal is “I want the cleanest, lowest-effort catch-all possible,” the Citi Double Cash is tough to beat.

Chase Freedom Unlimited: Category Juice With a Lower Floor

As a pure catch-all, the Chase Freedom Unlimited is falling behind the curve. It is really more of a part catch-all, part category card.

The baseline is 1.5% back on everything, with bonus categories like 3% on dining and 3% on drugstores. In my opinion, this card is the weakest of the three as a standalone catch-all. However, the synergies inside the Chase ecosystem are real, even if some of the multipliers overlap with other Chase cards. And like Citi, you can convert that cash back to Ultimate Rewards points by pairing it with a transferable card like the Sapphire Preferred.

If you want a no-fee card with a few stronger category earners and you are building a Chase stack, the CFU makes sense. But strictly as a no-fee catch-all, it ranks third.

The Decision Framework

Here is how to think about it:

Choose Bilt Blue if: You route your housing spend (rent or mortgage) through Bilt, you are willing to use Bilt Cash to unlock housing points, and your non-housing spend is at or under 75% of your housing payment. In this scenario, you are earning an effective 2.33X on your spend, with access to premium transfer partners. That is the best rate in the no-fee catch-all space.

Choose Citi Double Cash if: You do not have housing to unlock, or you want something you never have to think about. Flat 2% on everything. No tricks, no conditions. The safest answer for simplicity.

Choose Chase Freedom Unlimited if: You want a no-fee card with a few stronger categories and you are building out a Chase ecosystem. The 1.5% floor is lower than Citi’s 2%, but the bonus categories and Chase integration add value if you have the right pairing cards.

The Bilt Blue is not the best card for everyone. But for the right person, someone routing housing spend through Bilt with disciplined non-housing spend under the 75% threshold, it is ridiculously efficient. No other $0 card gets you 2.33X effective with Hyatt and Alaska transfer access. The math does not lie.

If you want free tools to run these numbers for your own spend across any cards, I built a Credit Card ROI Calculator for exactly this. Get it here

Best For / Not For

Who Should Get the Bilt Blue Card

Best for:

- Anyone willing to route their housing spend (rent or mortgage) through Bilt and earn points on it for $0 annual fee

- People whose non-housing monthly spend is at or under 75% of their housing payment, keeping the 2.33X effective rate clean

- Points optimizers who value transfer partner access to Hyatt, Alaska Airlines, and Aeroplan without paying an annual fee

- Anyone looking for the highest effective earn rate among no-fee catch-all cards, as long as they are willing to manage the Bilt Cash system

Who Should Pass on the Bilt Blue Card

Not for:

- Anyone carrying credit card debt. Pay that off first, then come back to credit card strategy

- People who want a simple “swipe and forget” catch-all with no portals or unlock mechanics to track

- Spenders whose non-housing spend significantly exceeds their housing payment, this changes the clean 2.33X math

- Cardholders who do not pay rent or mortgage through Bilt, since the housing unlock is the entire value driver

If you are newer to credit cards and not sure whether a strategy card like Bilt is the right starting point, the Wells Fargo Autograph is another strong no-fee option with simpler earning and transfer partner access.

The Bilt Blue Card earns an effective 2.33X on non-housing spend for anyone who routes housing spend through Bilt and uses the Bilt Cash unlock system, and it does it for $0 annual fee with 1:1 transfer partners like Hyatt and Alaska. For the right person, no other free catch-all comes close. For everyone else, the Citi Double Cash at flat 2% is the safer, simpler answer.

Bilt Blue Card Rating: 3.8/5 — Top-tier math for anyone routing housing through Bilt, held back by complexity and the narrow sweet spot that makes the strategy work.

Final Thoughts

The Bilt Blue Card is not a card you should grab because you saw a headline about 2.33X points. It is a card that works when you understand the conditions, run the numbers for your own spend, and commit to using the Bilt Cash system the right way.

For anyone routing housing through Bilt in the sweet spot, the effective earn rate beats every other $0 catch-all in the market right now. For everyone else, keep it simple: the Citi Double Cash or Chase Freedom Unlimited will serve you well without the overhead.

What is your take? Is the Bilt Blue worth the complexity, or is 2% flat the smarter play? Drop a comment and let me know.

Bilt Credit Card FAQs

Is the Bilt Blue Card worth it?

For anyone who routes housing spend (rent or mortgage) through Bilt and has non-housing spend under 75% of their housing payment, yes. The effective 2.33X earn rate on everyday spend with access to premium transfer partners like Hyatt and Alaska Airlines is the best value in the no-fee catch-all space. If you do not route housing through Bilt, the strategy does not work and you are better off with the Citi Double Cash at 2%.

How does Bilt Cash work to unlock points on housing?

You earn 4% Bilt Cash on non-housing purchases when you select the Flexible Bilt Cash option in the Bilt app. Every $30 in Bilt Cash unlocks 1,000 Bilt points on your rent or mortgage payment. The Bilt Cash essentially converts your everyday spending into bonus points on your biggest monthly bill.

Is the Bilt Blue Card better than the Citi Double Cash?

It depends on whether you route housing through Bilt. If you do, and your non-housing spend stays under 75% of your housing payment, the Bilt Blue’s effective 2.33X beats the Citi Double Cash’s flat 2%. If you do not have housing to unlock, the Citi Double Cash wins on simplicity and requires zero management. Both are strong, but they serve different spending profiles.

What are Bilt points worth?

Bilt points value depends on how you redeem them. Transferred 1:1 to partners like Hyatt, you can get 1.5 to 2.5 cents per point on hotel redemptions (as of April 2026). Transferred to Alaska Airlines, domestic flights can yield similar value. Cash back redemptions are worth significantly less. The transfer partners are where the real value lives.

Can you use the Bilt Blue Card without paying rent?

Technically yes. You would just need to use your Bilt Cash in other ways in Bilt’s portal. It could still be valuable but the math gets messier to know if it is truly beating the standard 2% catch-all.

Bilt Blue

Earns points on rent with no annual fee. 1x everyday or 4% Bilt Cash (flexible). Up to 1.25x on housing.

$0/yr

Bilt Obsidian Black

3x dining or grocery (select annually), 2x travel. $100/yr Bilt Hotel credit. 4% Bilt Cash flexible. Up to 1.25x housing.

$95/yr

Bilt Palladium

2x everyday, 4% Bilt Cash flexible. $400/yr hotel credit, $200 Bilt Cash, Priority Pass. Up to 1.25x housing.

$495/yr

Chase Freedom Unlimited

5% Chase Travel, 3% dining and drugstores, 1.5% everything else.

$0/yr

Citi Double Cash

Flat 2% on everything (1% when you buy + 1% when you pay).

$0/yr

Citi Strata Premier

3x on restaurants, supermarkets, gas/EV, air travel, hotels. 10x via Citi Travel portal. Transfer partners.

$95/yr

Wells Fargo Autograph

3x on restaurants, travel, gas, transit, streaming, phone plans. Transfer partners.

$0/yrTerms apply. Some links are affiliate links. I only recommend products I personally use or genuinely believe will help you. Pay your balance in full.

Some links in this article are affiliate links. I only recommend products I personally use or genuinely believe will help you. Terms apply. Pay your balance in full. Applying for a credit card results in a hard inquiry. I’m not a financial advisor or CPA. This is personal experience and opinion.